You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

Scottish Widows Retirement Expert

Research from Scottish Widows’ latest Retirement Report highlights the impact of poor physical and mental health on people’s ability to work and prepare for retirement.

While three in five UK adults (60%) expect to be fit enough to continue working until their planned retirement age, three in 10 (29%) have seen their work impacted due to their physical or mental health over the past five years.

For some, this has led to significant changes in working patterns, including stopping work altogether (10%), reducing working hours (7%) or moving into less demanding or lower-paid roles (6%).

Health doesn’t just affect working life - it shapes retirement outcomes too. Lower earnings and disrupted careers can reduce pension contributions, limit savings, and make it harder to budget and plan confidently for the future.

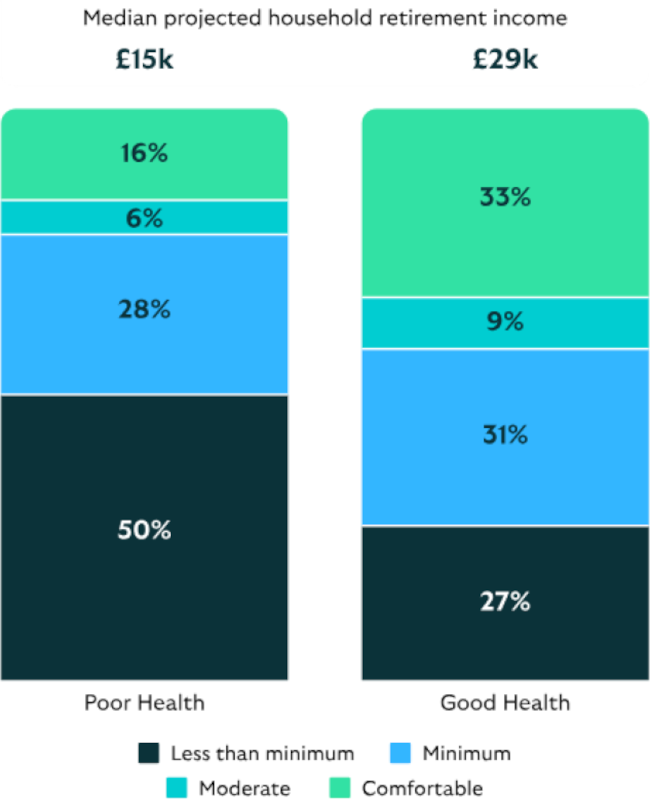

Half (50%) of UK adults with physical or mental health conditions that impact their day-to-day lives face pension poverty, according to the latest National Retirement Forecast (NRF) projections*. This is double the rate of the general population (27%).

The report also highlights a gap in preparing for later-life care. A third (34%) of adults have not yet considered care needs in later life, while over half (51%) are not confident they would be able to afford care if required.

The picture is even more concerning for those living with a mental or physical health condition, among whom two-thirds (67%) lack confidence in their ability to pay for any care they may need in later life.

Susan Hope, pension expert at Scottish Widows, commented: “Navigating health challenges is something which many of us will have to face in our later years. Whether it's managing a chronic condition, mental burnout, or working through menopause, physical and emotional struggles often force people to change their working patterns, cut back their hours or drop out of the workforce altogether.

“This just doesn’t affect our day-to-day lives, it often knocks our long-term financial plans off track too. The good news is that you don’t need to completely overhaul your life today to make a meaningful difference for tomorrow. Small changes really do add up. Taking just ten minutes to check your pension balance, using an online calculator to see what you might need, or finding out if your employer matches extra contributions can give you more control.”

Download full press release (PDF, 185KB)

Methodology

The research was conducted online by YouGov across a total 6,224 adults aged 18+, weighted to be representative of the UK population, and including a boost of 1,000 adults aged 18+ to better understand the retirement prospects of minority ethnic groups, also weighted to be representative of the UK minority ethnic population aged 18+. Fieldwork was carried out between 16 February 2026 and 24 February 2026.

*The National Retirement Forecast (NRF), first run in our 2023 Retirement Report with Frontier Economics, projects retirement outcomes for those aged 22 to 65 based on savings, behaviours and income sources, comparing expected income to potential living and housing costs in retirement. The NRF is based on data from approximately 6,000 people.

Pensions UK’s: Retirement Living Standards (RLS). These standards outline the income thresholds for different retirement lifestyles (“minimum”, “moderate” and “comfortable”) showing how much can be afforded for singles and couples, living inside and outside of London, in retirement across different categories of spending such as clothing, transportation, holidays, and home maintenance.

About Scottish Widows

Founded in 1815, Scottish Widows is part of Lloyds Banking Group, the UK’s largest digital bank and financial services group. With £280bn in total assets under administration and more than six million customers, Scottish Widows’ award-winning product range includes workplace and individual pensions, annuities, life cover, critical illness and income protection, as well as savings and investment products.

Scottish Widows has more than 1.75m digitally registered customers. The Scottish Widows Platform is trusted by more than 18,000 advisers and 5,400 advice firms, which manage the pensions and investments of almost 166,000 clients. .