You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

When you save into a pension you usually get tax relief from the government. And, the money you earn from your pension investments is not affected by UK Capital Gains Tax (CGT).

This means more of your money is protected from tax and kept for your retirement. And because of tax relief, paying into a pension could also cost you less than other tax-efficient investment options like Individual Savings Accounts (ISAs).

The more time your money is invested, the more time it has to grow, so it’s a good idea to start paying into a pension as early as possible. And it’s never too late to start.

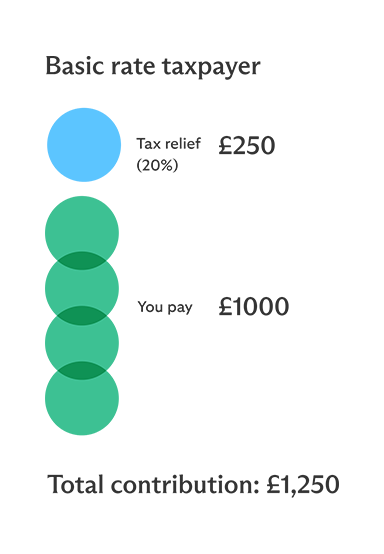

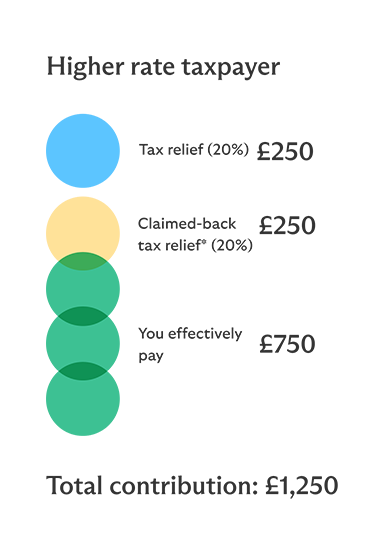

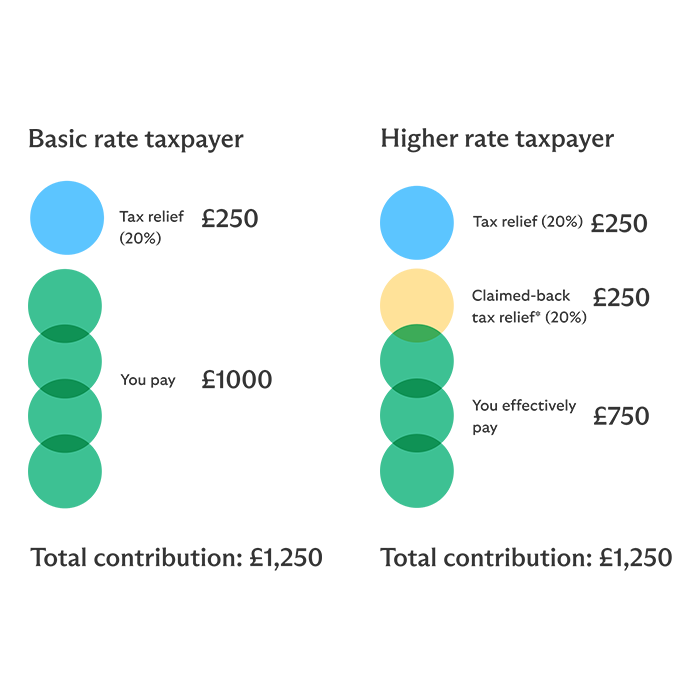

Here’s an example to show how tax relief works if you wanted to contribute a total of £1,250 into a personal pension.

*You initially pay £1000 into your pension. By claiming back the additional 20% higher rate tax relief through self-assessment, this effectively means you’ve only paid £750 towards a £1,250 total pension contribution. If you live in Scotland, or are an additional rate taxpayer, the reclaimed tax amount could be more.

This is why higher and additional rate taxpayers, who are saving into a personal pension, should remember to complete a Self-Assessment to claim back the tax relief they’re entitled to.

|

Band |

Taxable income |

Tax rate |

|---|---|---|

|

Band Personal allowance |

Taxable income Up to £12, 570 |

Tax rate 0% |

|

Band Basic rate |

Taxable income £12,571 to £50,270 |

Tax rate 20% |

|

Band Higher rate |

Taxable income £50, 271 to £125,140 |

Tax rate 40% |

|

Band Additional rate |

Taxable income Over £125,140 |

Tax rate 45% |

How you get tax relief added back into your pension pot depends on the type of pension you have.

Personal pensions, including Group Personal Pensions and Group SIPP

If you have a personal pension, because you’ve already been taxed on the income you’re paying in, it needs to be added back. Your pension provider claims back the basic rate of 20% tax relief for you from HMRC. It happens automatically so there’s nothing for you to do.

Higher or additional rate taxpayers in England, Wales and Northern Ireland can claim back the additional tax through Self-Assessment. There are different rules around income tax in Scotland.

Occupational pensions, including Master Trust pensions

Your employer takes your pension payments from your salary before you pay tax, and you only pay tax on what is left. Your employer does this for you and it shows in your pay cheque. This means you get the right level of tax relief, no matter which tax band you are in, without having to claim anything back from HMRC. If you’re not sure, talk to your employer.

Your annual allowance is the limit on how much you or anyone else paying into a pension on your behalf (for example your employer) can pay into it without a tax charge.

For the current tax year, the annual allowance is £60,000.

If you earn less than £60,000

Your allowance of how much you can contribute to your pension to be eligible for tax relief is either:

The annual allowance resets each tax year. It’s also possible to ‘carry forward’ the last 3 years’ of the annual allowance to add to this year’s. You’ll need to contact HMRC to do this.

If you flexibly access your pension

This will trigger the Money Purchase Annual Allowance (MPAA) which is currently set at £10,000. Your pension provider will tell you if you’re affected by the MPAA. You’ll need to tell your other pension providers within 91 days or you could get a fine.

If you’re a very high earner

You’ll also have a reduced annual allowance, called the Tapered Annual Allowance. This applies if your annual income is over £200,000, not including:

This is known as your threshold income.

If your threshold income is above this, check if your annual income is over £260,000, including:

This is known as your adjusted income.

If your adjusted income is above £260,000, your annual allowance goes down by £1 for every £2 over £260,000.

The lowest your annual allowance can be reduced to is £10,000.

For more information, talk to a financial adviser. There’s usually a charge for financial advice. You can also find more information about tapered annual allowances at Money Helper.

The Scottish Widows Self-Invested Personal Pension is provided by Embark Investment Services Limited, a company incorporated in England and Wales (company number 09955930) with its registered office at 33 Old Broad Street, London EC2N 1HZ. Embark Investment Services Limited is authorised and regulated by the Financial Conduct Authority (Financial Services Register number 737356).

Dealing and stockbroking administration services for the Scottish Widows SIPP are provided by Halifax Share Dealing Limited (HSDL), which is a wholly owned subsidiary of Embark Group Limited and part of Lloyds Banking Group. HSDL is a company incorporated in England and Wales (company number 3195646) with its registered office at: Trinity Road, Halifax, West Yorkshire, HX1 2RG. HSDL is authorised and regulated by the Financial Conduct Authority (Financial Services Register number 183332). HSDL is a member of the London Stock Exchange and an HM Revenue & Customs Approved ISA Manager.

A simple, powerful way to save for retirement - without the guesswork.

Take control of how your personal pension savings are invested.

Lots of us have pensions from old jobs. Bringing them together could make life easier.

Find a personal pension that’s right for your retirement goals.

Find a personal pension that’s right for your retirement goals.