You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

Head of Asset Allocation and Research

The start of a new tax year can be a good time to think about investing options, like ISAs for example. But many people worry about when to invest, particularly when financial markets have been volatile. Should you wait for the ‘right time’ or invest as soon as you can? In this article, we’ll look at:

At its simplest, ‘timing the market’ means that you try to buy investments when they’re trading at their lowest point, and sell them at their highest - helping you make the best return. This can be particularly tempting during periods of market volatility or uncertainty.

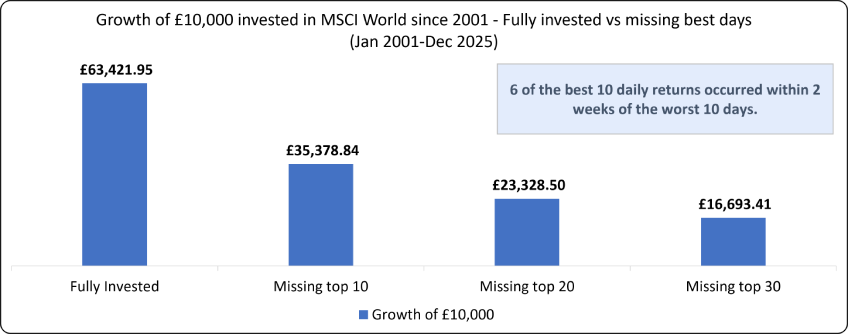

The challenge is that markets can be unpredictable and can react quickly or not at all to news. That makes it hard to know if stocks are at their lowest level, or if they’ve peaked. It’s a dilemma that even professional investors can struggle to get right consistently.

Some factors that make timing the market difficult are:

It means investing early and staying invested for the long term rather than trying to predict short-term movements. This allows your investments time to grow and means you can benefit from compounding. Simply put, the longer your money is invested, the more chance it has to grow on top of any growth it’s already achieved.

Time in the market can help you unlock the power of long-term investing. It can help smooth out short-term volatility, or the normal ups and downs of financial markets. If we look at past periods of volatility, we can see that patient investors are typically rewarded over the long run by sticking to their long-term investing plans and resisting the urge to react to news headlines.

Regular investing is another way to take some of the worry out of market timing. Rather than investing a large amount all at once, you invest smaller amounts on a regular basis - for example, monthly contributions into your ISA.

This means your money is invested at different market levels over time. When prices are higher, your money buys fewer investments; when prices are lower, it buys more. Over time, this can help reduce the risk of investing everything at a market high.

For many people, especially those making monthly ISA contributions, this approach can turn market volatility from something to fear into something that simply becomes part of their investing journey.

There’s no ‘right’ way to invest and everyone’s situation and motivation is different. But there are some areas to consider:

It’s fine to start cautiously and stay cautious, or you might find your confidence builds over time.

You can’t control market movements, but you can control:

Focussing on your long‑term goals rather than short‑term noise, means you can make more considered decisions.