You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

Head of Pensions Policy, Scottish Widows

Under the latest National Retirement Forecast (NRF) projections*, a third of UK adults face poverty in retirement, according to Scottish Widows’ latest annual Retirement Report.

The NRF projects retirement outcomes based on savings, behaviours and income sources, comparing expected income to potential living and housing costs in retirement.

The report shows a marked reduction in the number of people on track for a less than minimum retirement lifestyle - 31% (12.2 million people) - down from 39% (15.3 million) in 2025. However, the current state of the nation's savings is still precarious.

The positive change has been driven by two key factors. Firstly, those not saving in the traditional way through a pension have increased their level of savings elsewhere, and more of those also now expect to own their own home when they retire.

Secondly, falling energy costs in the short-term have led to more people meeting the minimum lifestyle standard as set out by Pensions UK’s Retirement Living Standards**. However, with recent global events pushing energy costs back on an upward trajectory, this positive progress could soon be undone.

Pete Glancy, head of pension policy at Scottish Widows, said: “This report paints a complex picture. While the fall in pension poverty compared to a year ago is a step in the right direction, this shift in retirement fortunes is complex and the current state of the nation's savings is still polarised. The factors we can control, like how much we save or how much we expect to receive in retirement, may improve, but can easily be thrown off course by shifting external factors like increases to energy and general cost of living.”

The UK Government’s recently established Pensions Commission is expected to recommend changes which government and industry should implement during the 30s and 40s - to put the nation in good shape for retirement through the second half of the century.

Even if the recommendations of the Pensions Commission are adopted by the Government and implemented, it will be many decades until the full benefits are felt. In the meantime, most of the population won’t have enough in their pension pots to facilitate their retirement, and it will be necessary for them to consider other savings, investments and housing equity in totality.

Scottish Widows recommends the following policy measures to improve retirement saving prospects in the UK:

Automatic enrolment is an important tool to help more people have at least a basic lifestyle in retirement, especially for those on low to middle incomes.

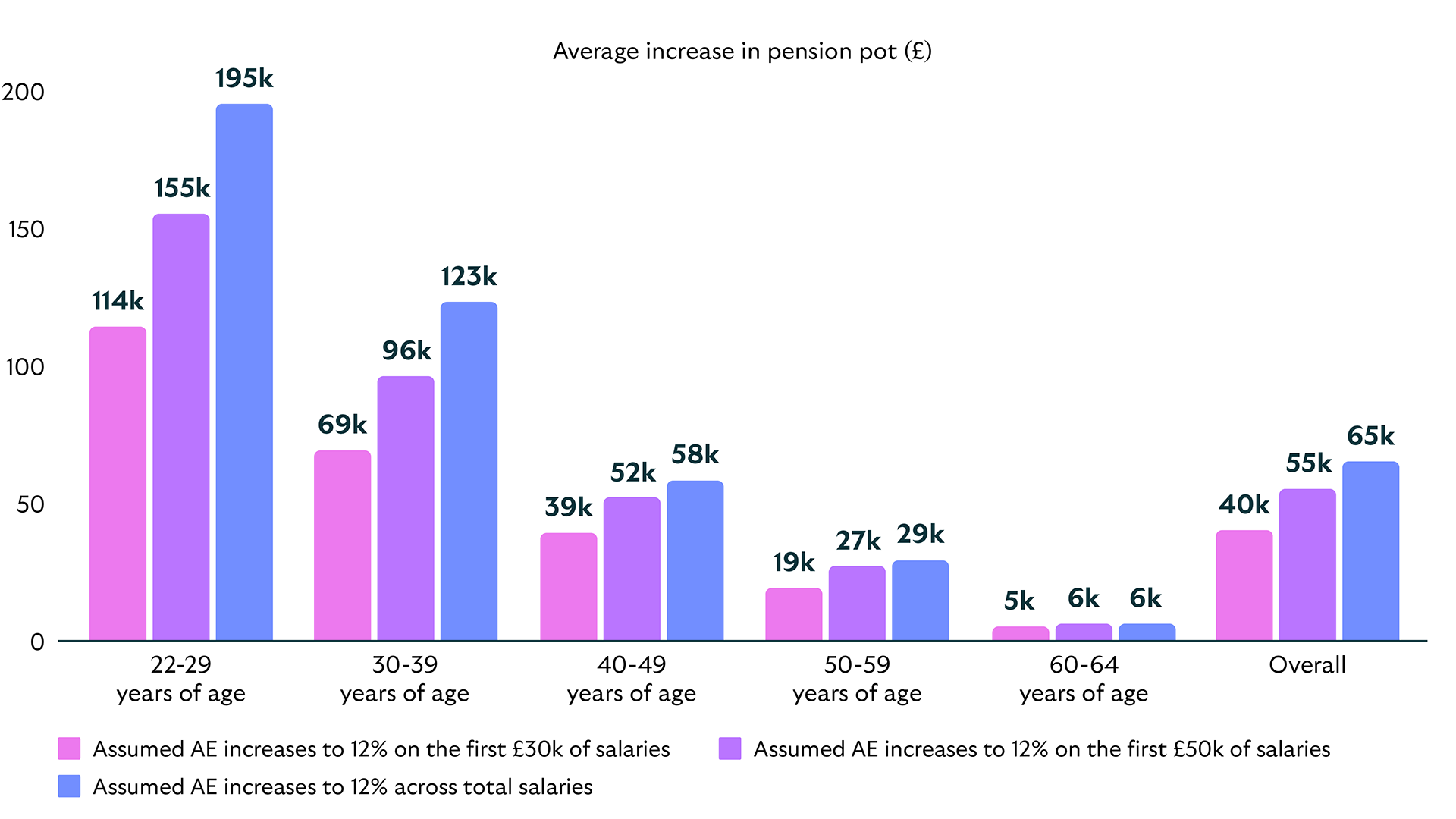

Scottish Widows calculates that increasing default contribution (DC) rates would have a sizable impact on the pension pots of those currently saving, especially for young people. Raising total contribution rates from 8% to 12% on the first £30k of salary would increase projected retirement savings by £40k on average. For those aged 22–29, the impact is far greater, increasing pots to around £114k at retirement.

Increasing default contribution rates has the largest impact on the size of pension pots for younger cohort and those who will join the workforce in the future

Scottish Widows’ analysis also shows that among defined contribution (DC) members saving below 12%, should the statutory level of contribution through auto-enrolment increase from 8% to 12% across total salaries - it would drastically reduce pension poverty from 32% to 13% - an increase of £65k. If the increase were applied only to the first £50k of salary the average pot would increase by £55k, with pensioner poverty also being reduced dramatically to 14%.

The remaining 13% at risk of pension poverty are mainly self-employed, part-time or unemployed people.

Extending auto-enrolment could significantly improve the nation’s retirement outcomes; this is especially important as the UK’s 4.39 million self-employed and many of the 8.79 million part-time workers**** - currently excluded from auto-enrolment - are more likely to face pension poverty, with around a third in each group experiencing a below-minimum retirement lifestyle.

Pete added: “The way people are working continues to evolve, but our retirement system still lags behind. This year we have modelled the impact of some policy changes only on the youngest workers as this gives us the best indication of the long-term benefit applying not only to them, but all future generations yet to join the workforce.

“We must also ensure that choosing flexibility today - through self-employment or part-time work - doesn’t come at the expense of tomorrow. Extending auto-enrolment to the self-employed, as is one of our recommendations to the Pension Commission, is critical and should be implemented at pace to close this gap in retirement saving.

“Most people are unlikely to have enough in their pension pots alone to fund their desired retirement, so pensions can no longer be viewed in isolation. Considering pensions alongside other savings, investments and housing wealth - and advancing the Government’s Open Finance agenda - will be key to improving retirement outcomes for all.”

Download full press release (PDF, 203KB)

The research was conducted online by YouGov across a total 6,224 adults aged 18+, weighted to be representative of the UK population, and including a boost of 1,000 adults aged 18+ to better understand the retirement prospects of minority ethnic groups, also weighted to be representative of the UK minority ethnic population aged 18+. Fieldwork was carried out between 16 February 2026 and 24 February 2026.

*The National Retirement Forecast (NRF), first run in our 2023 Retirement Report with Frontier Economics, projects retirement outcomes for those aged 22 to 65 based on savings, behaviours and income sources, comparing expected income to potential living and housing costs in retirement. The NRF is based on data from approximately 6,000 people.

**Pensions UK’s: Retirement Living Standards (RLS). These standards outline the income thresholds for different retirement lifestyles (“minimum”, “moderate” and “comfortable”) showing how much can be afforded for singles and couples, living inside and outside of London, in retirement across different categories of spending such as clothing, transportation, holidays, and home maintenance.

***The chart shows the increase in projected pension pot at retirement by age band for DC members contributing at or below new proposed AE levels:

The pink bars project AE increases to 12% on the first £30k of salaries

The purple bars project AE increases to 12% on the first £50k of salaries

The blue bars project AE increases to 12% across total salaries

****https://researchbriefings.files.parliament.uk/documents/CBP-9366/CBP-9366.pdf

Founded in 1815, Scottish Widows is part of Lloyds Banking Group, the UK’s largest digital bank and financial services group. With more than £232bn assets under administration and more than 6 million customers, Scottish Widows’ award-winning product range includes workplace and individual pensions, annuities, life cover, critical illness and income protection, as well as savings and investment products.

More than 2 million customers access Scottish Widows products and services through the Lloyds Bank and Scottish Widows apps, in addition to accessing directly through independent financial advisers. The Scottish Widows Platform is trusted by more than 18,000 advisers and 5,400 advice firms, which manage the pensions and investments of almost 166,000 clients.