You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

Buying small shares (units) of an investment fund. This means that your money is invested in listed companies and other assets, which can rise and fall in value.

Paying for your life cover.

Charges for managing your plan.

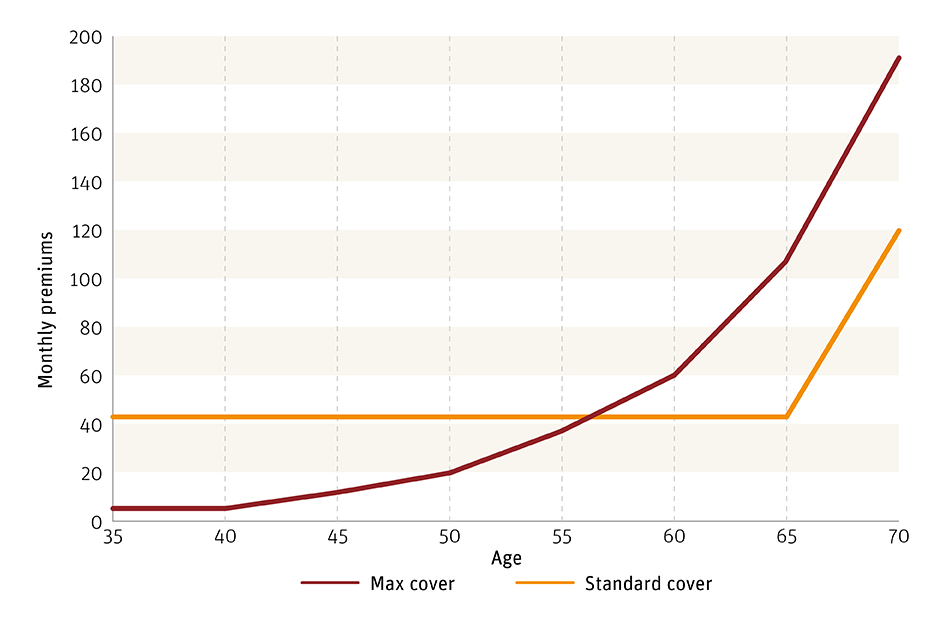

This is an example showing a sum assured of £100,000. For illustrative purposes only.