You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

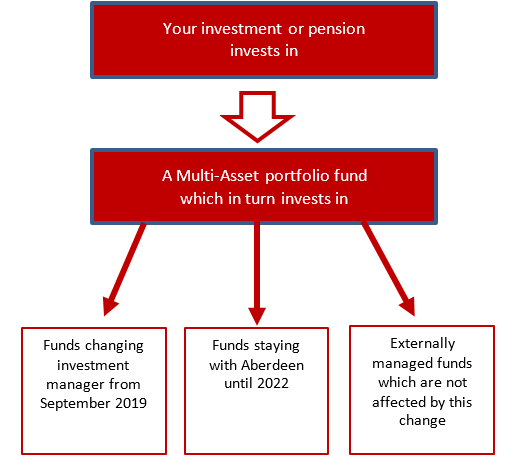

You can find all the changes that have previously been made here.

On 19th August, Schroders Personal Wealth (SPW) decided to change their Multi-Manager funds.

The change means SPW no longer uses third party investment managers for the Multi-Manager funds, and will instead manage the funds itself. They believe this approach is the most appropriate for delivering good long-term investment outcomes for investors.

We’re updating the Scottish Widows funds which, in turn, invest in these Multi-Manager funds, to reflect the change. Specifically, we’re changing the funds names and aims.

We’ll write to you if you're invested in these funds. You don’t need to do anything, as the changes will happen automatically. You can choose your own investment option any time by calling us.

The CM Boston Company US Opportunities fund (“the fund”) previously invested in BNY Mellon US Opportunities Fund Sterling Income Shares Inc (“the underlying fund”).

On 7th September, BNY Mellon merged the underlying fund with another underlying fund, the BNY Mellon US Equity Income fund. The charges for the fund, and the overall risk profile, remain the same.

BNY Mellon believes the merger is in the best interests of the underlying funds’ investors and places investors’ money in a fund which provides better value, lower risk, and historically better performance. Please note, however, that past performance is not a guide to future performance, and fund performance can fluctuate over time.

We’ll write to you if you’re invested in this fund. You don’t need to do anything if you believe the fund will continue to meet your investment needs. You can move your investment to another fund or funds of your choice at any time.

The results of the Extraordinary General Meetings which took place on 4th September 2024 at Scottish Widows, Port Hamilton, 69 Morrison Street, Edinburgh, EH3 8YF, are shown below.

Eleven of the twelve fund merger proposals were approved by the investors’ vote. The Regional mergers into the receiving funds took on 21st October 2024. The UK mergers into the receiving funds took place on 18th November 2024.

The North American Fund, a sub-fund of HBOS International Investment Funds ICVC, proposal to merge was not approved by the investors’ vote. As a result, we’ll re-consider the options available to the fund.

|

Regional Merging Fund |

Receiving Fund |

Proposal Carried |

Minutes of the EGM |

|---|---|---|---|

|

Regional Merging Fund American Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Receiving Fund Global Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 79KB) |

|

Regional Merging Fund European Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Receiving Fund Global Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 77KB) |

|

Regional Merging Fund Japan Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Receiving Fund Global Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 77KB) |

|

Regional Merging Fund Pacific Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Receiving Fund Global Growth Fund A sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 77KB) |

|

Regional Merging Fund European Fund A sub-fund of HBOS International Investment Funds ICVC |

Receiving Fund International Growth Fund A sub-fund of HBOS International Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 78KB) |

|

Regional Merging Fund Far Eastern Fund A sub-fund of HBOS International Investment Funds ICVC |

Receiving Fund International Growth Fund A sub-fund of HBOS International Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 78KB) |

|

Regional Merging Fund Japanese Fund A sub-fund of HBOS International Investment Funds ICVC |

Receiving Fund International Growth Fund A sub-fund of HBOS International Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 78KB) |

|

Regional Merging Fund North American Fund A sub-fund of HBOS International Investment Funds ICVC |

Receiving Fund International Growth Fund A sub-fund of HBOS International Investment Funds ICVC |

Proposal Carried No |

Minutes of the EGM View Document (PDF, 78KB) |

|

UK Merging Fund |

Receiving Fund |

Proposal Carried |

Minutes of the EGM |

|---|---|---|---|

|

UK Merging Fund UK Equity Income Fund A sub-fund of Scottish Widows UK and Income Investment Funds ICVC |

Receiving Fund UK Equity Tracker Fund A sub-fund of Scottish Widows Tracker and Specialist Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 77KB) |

|

UK Merging Fund UK Growth Fund A sub-fund of Scottish Widows UK and Income Investment Funds ICVC |

Receiving Fund UK Equity Tracker Fund A sub-fund of Scottish Widows Tracker and Specialist Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 77KB) |

|

UK Merging Fund UK Equity Income Fund A sub-fund of HBOS UK Investment Funds ICVC |

Receiving Fund UK Equity Tracker Fund A sub-fund of HBOS UK Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 78KB) |

|

UK Merging Fund UK Growth Fund A sub-fund of HBOS UK Investment Funds ICVC |

Receiving Fund UK Equity Tracker Fund A sub-fund of HBOS UK Investment Funds ICVC |

Proposal Carried Yes |

Minutes of the EGM View Document (PDF, 79KB) |

We’re making changes to some of our Life and Pension Funds which currently invest in funds that hold investments overseas and in the UK.

What this means for some of our Life and Pension Funds investing in a fund that holds overseas investments

Our impacted Life and Pension Funds will move to invest in a different fund - either the Scottish Widows Unit Trust Managers Limited Global Growth Fund or the HBOS Investment Managers Limited International Growth Fund.

From 21st October 2024 these life and pension funds will have new investment aims (PDF, 173KB) and their names will change (PDF, 143KB). Customers may continue to see the old fund name on communications we send them until the names are updated.

What this means for some of our Life and Pension Funds investing in a fund that holds UK investments

Our impacted Life and Pension UK funds will move to invest a different fund - either the Scottish Widows Unit Trust Managers Limited UK Equity Tracker Fund or the HBOS Investment Managers Limited UK Equity Tracker Fund.

The funds will change from being actively managed, and aiming to outperform its benchmark index, to being passively managed and aiming to track its benchmark index.

The fund manager (also known as an investment adviser) will change from Schroders to BlackRock.

From 18th November 2024 these life and pension funds will have new investment aims (PDF, 151KB) and their names will change (PDF, 131KB). You may continue to see the old fund name on communications we send you.

Customer notification for customers in our UK Life and Pension Funds

We’re writing to our customers invested in one or more of these life and pension funds to let them know about these changes, and to ask them to review how the life and pension funds will be invested, to make sure that the funds continue to meet their investment needs.

The Ethical Fund in the HBOS Specialised Investment Funds ICVC operated by HBOS Investment Fund Managers Limited was identified as one we proposed to close by merger into an alternative fund. See March 2024: Proposed Fund changes.

However, investors in the fund didn’t approve the proposal to merge the Ethical Fund with the International Growth Fund, so we’re now going to close the Ethical Fund in October 2024.

We’re writing to those affected by the Ethical Fund closure to explain their options and we’re asking them to please let us know what they’d like to do with their investment in the closing Ethical Fund on or before 14th October 2024.

The transaction costs incurred in selling the Fund’s assets will be paid for by the Fund and are estimated to be 0.03% of the current net asset value of the Fund. The other costs and expenses of closing the Fund will be paid for by us.

The Scottish Widows Multi-Manager UK Equity Income Fund and Scottish Widows Multi-Manager Global Real Estate Fund CS8 are closing. These funds invest in underlying funds managed by Schroders Personal Wealth (SPW). SPW has decided to close the underlying funds, so we’re closing the funds that invest in them.

We’ll write to you if you’re invested in these funds. If you don’t contact us to choose a new fund or funds to invest in, from 13th August we’ll move the value of your investment from the closing funds into one of the following funds:

We've given more information about the replacement funds and other investment options available to your plan, including their aims, risks and charges.

From 19th August, we’re changing the underlying fund the Scottish Widows Multi-Manager Global Real Estate Securities Fund invests in, from the SPW Multi-Manager Global Real Estate Securities Fund to the iShares Environment & Low Carbon Tilt Real Estate Index Fund.

We’ll also change the name of the fund from the Scottish Widows Multi-Manager Global Real Estate Securities Fund to the SW iShares Environment & Low Carbon Tilt Real Estate Index Fund.

Any regular payments to the fund will continue to be invested as usual.

We’ll write to you if you’re invested in this underlying fund. You don’t need to do anything if you believe the fund will continue to meet your investment needs. You can move your investment to another fund or funds of your choice at any time.

The investment aim of the Fund, and the updated Fund are shown below.

Scottish Widows Multi-Manager Global Real Estate Securities Fund (current Fund) - Fund Aim

The fund aims to achieve long-term growth by investing principally in a globally diversified portfolio of shares of listed companies, real estate investment trusts (REITs) and other investments, the activities of which include the ownership, management and/or development of global real estate. The portfolio’s investments will be managed by a number of fund managers. Fund managers are selected and assets are allocated in conjunction with Russell Investment Group.

SW iShares Environment & Low Carbon Tilt Real Estate Index Fund (updated Fund) - Fund Aim

The aim of the Fund is to provide a return on your investment (generated through an increase in the value of the assets held by the Fund) by tracking closely the performance of the FTSE EPRA/NAREIT Green Low Carbon Target Index. (the “Benchmark Index”). Although the Fund aims to achieve its investment objective, there is no guarantee that this will be achieved. The Fund’s capital is at risk meaning that the Fund could suffer a decrease in value and the value of your investment would decrease as a result.

Proposed OEIC and ISA Fund changes – Regional Funds

Following review and discussion with Schroder Investment Management Limited, the investment adviser of the Funds, we remain confident in the investment strategy for the eight Regional funds listed below but believe they would benefit from investment through global markets. We are therefore proposing fund mergers to investors in these eight Regional funds.

| Regional Merging Funds | ICVC | Receiving Fund Name | ICVC |

|---|---|---|---|

American Growth |

Scottish Widows Overseas Growth Investment Funds ICVC | Global Growth | Scottish Widows Overseas Growth Investment Funds ICVC |

| European Growth | Scottish Widows Overseas Growth Investment Funds ICVC | Global Growth | Scottish Widows Overseas Growth Investment Funds ICVC |

| Japan Growth | Scottish Widows Overseas Growth Investment Funds ICVC | Global Growth | Scottish Widows Overseas Growth Investment Funds ICVC |

| Pacific Growth | Scottish Widows Overseas Growth Investment Funds ICVC | Global Growth | Scottish Widows Overseas Growth Investment Funds ICVC |

| European | HBOS International Investment Funds ICVC | International Growth | HBOS International Investment Funds ICVC |

| Far Eastern | HBOS International Investment Funds ICVC | International Growth | HBOS International Investment Funds ICVC |

| Japanese | HBOS International Investment Funds ICVC | International Growth | HBOS International Investment Funds ICVC |

| North American | HBOS International Investment Funds ICVC | International Growth | HBOS International Investment Funds ICVC |

Following a review of our fund range as part of our 2022 Assessment of Value report, we’ve considered the options to improve outcomes for investors. We are therefore proposing fund mergers to investors in the four UK Funds listed below.

On 7th October 2024, BlackRock will be appointed as the investment adviser of the UK Merging funds in place of Schroders.

| UK Merging Funds | ICVC | Receiving Fund Name | ICVC |

|---|---|---|---|

UK Equity Income |

Scottish Widows UK and Income Investment Funds ICVC | UK Equity Tracker | Scottish Widows Tracker and Specialist Investment Funds ICVC |

| UK Growth | Scottish Widows UK and Income Investment Funds ICVC | UK Equity Tracker | Scottish Widows Tracker and Specialist Investment Funds ICVC |

| UK Equity Income | HBOS UK Investment Funds ICVC | UK Equity Tracker | HBOS UK Investment Funds ICVC |

| UK Growth | HBOS UK Investment Funds ICVC | UK Equity Tracker | HBOS UK Investment Funds ICVC |

These proposed changes require approval from OEIC and ISA investors in the funds. We’re mailing investors with details of the change and asking them to vote. To make the proposed changes, we need approval from 75% of the investors who vote.

If investors approve the proposal:

We don’t expect that the merger will constitute a disposal of Shares in the Merging Fund for UK capital gains tax purposes. Relevant clearances from HMRC have been received.

The tables below provide key dates along with links to the relevant Voting Documents which provide detailed information on our proposed changes.

Detailed Fund Information

To access the latest investment documentation for the funds, for example Key Investor Information Documents (KIIDs), Supplementary Investor Information Documents (SIIDs) and prospectuses please visit:

Scottish Widows funds

Halifax funds.

You can find the new KIID for the Scottish Widows UK Equity Tracker Fund Class A Accumulation fund here (PDF, 852KB).

| Regional Merging Funds | ICVC | Voting Document | EMG Date and Time |

|---|---|---|---|

American Growth |

Scottish Widows Overseas Growth Investment Funds ICVC | 38166 (PDF, 341KB) | 10:50 AM on 4th September 2024 |

| European Growth | Scottish Widows Overseas Growth Investment Funds ICVC | 38165 (PDF, 341KB) | 10:40 AM on 4th September 2024 |

| Japan Growth | Scottish Widows Overseas Growth Investment Funds ICVC | 38162 (PDF, 340KB) | 10:30 AM on 4th September 2024 |

| Pacific Growth | Scottish Widows Overseas Growth Investment Funds ICVC | 38161 (PDF, 341KB) | 10:20 AM on 4th September 2024 |

| European | HBOS International Investment Funds ICVC | 38163 (PDF, 309KB) | 11:40 AM on 4th September 2024 |

| Far Eastern | HBOS International Investment Funds ICVC | 38160 (PDF, 308KB) | 11:30 AM on 4th September 2024 |

| Japanese | HBOS International Investment Funds ICVC | 38159 (PDF, 309KB) | 11:20 AM on 4th September 2024 |

| North American | HBOS International Investment Funds ICVC | 38164 (PDF, 309KB) | 11:50 AM on 4th September 2024 |

| UK Merging Funds | ICVC | Voting Document | EMG Date and Time |

|---|---|---|---|

UK Equity Income |

Scottish Widows UK and Income Investment Funds ICVC | 38156 (PDF, 360KB) | 10:00 AM on 4th September 2024 |

| UK Growth | Scottish Widows UK and Income Investment Funds ICVC | 38158 (PDF, 344KB) | 10:10 AM on 4th September 2024 |

| UK Equity Income | HBOS UK Investment Funds ICVC | 38155 (PDF, 326KB) | 11:00 AM on 4th September 2024 |

| UK Growth | HBOS UK Investment Funds ICVC | 38157 (PDF, 311KB) | 11:10 AM on 4th September 2024 |

The results of the Extraordinary General Meetings which took place on 18th April 2024 at Scottish Widows, Port Hamilton, 69 Morrison Street, Edinburgh, EH3 8YF, are shown below.

Eight of the nine fund merger proposals were approved by the investors’ vote. The mergers into the receiving funds took place on 24th June 2024.

The Ethical Fund, a sub-fund of HBOS Specialised Investment Funds ICVC, proposal to merge was not approved by the investors’ vote. As a result, the fund will be closed in due course.

| Merging Fund | Receiving Fund | Proposal Carried | Minutes of the EGM |

|---|---|---|---|

Smaller Companies Fund a sub-fund of HBOS Specialised Investment Funds ICVC |

UK Equity Tracker Fund a sub-fund of HBOS UK Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

| Special Situations Fund a sub-fund of HBOS Specialised Investment Funds ICVC |

UK Equity Tracker Fund a sub-fund of HBOS UK Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

| Fund of Investment Trusts a sub-fund of HBOS Specialised Investment Funds ICVC |

International Growth Fund a sub-fund of HBOS International Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

| Ethical Fund a sub-fund of HBOS Specialised Investment Funds ICVC |

International Growth Fund a sub-fund of HBOS International Investment Funds ICVC |

No | View document (PDF, 76KB) |

| UK Select Growth Fund a sub-fund of Scottish Widows UK and Income Investment Funds ICVC |

UK Equity Tracker Fund a sub-fund of Scottish Widows Tracker and Specialist Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

| UK Smaller Companies Fund a sub-fund of Scottish Widows Tracker and Specialist Investment Funds ICVC |

UK Equity Tracker Fund also a sub-fund of Scottish Widows Tracker and Specialist Investment Funds ICVC |

Yes | View document (PDF, 76KB) |

| European Select Growth Fund a sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Global Select Growth Fund also a sub-fund of Scottish Widows Overseas Growth Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

| Adventurous Growth Fund a sub-fund of Scottish Widows Income and Growth Funds ICVC |

Progressive Growth Fund also a sub-fund of Scottish Widows Income and Growth Funds ICVC |

Yes | View document (PDF, 77KB) |

| Ethical Fund a sub-fund of Scottish Widows UK and Income Investment Funds ICVC |

Environmental Investor Fund also a sub-fund of Scottish Widows UK and Income Investment Funds ICVC |

Yes | View document (PDF, 77KB) |

Japan’s financial markets close on various days throughout the year to mark national holidays. In 2024 the holidays fall on Monday 29th April and then 2 consecutive business days - Fri 3rd May and Mon 6th May 2024.

OEICS and ISAS

Our three Japanese OEIC funds, which invest exclusively in Japanese equities, will be unavailable for trading on these dates. These funds are:

Any investors in these OEICs, including those invested via an ISA, who want to buy or sell ahead of the first market closure should submit their instructions before the following cut off points:

| FUND NAME | DATE FOR CLIENT INSTRUCTION TO BE ACCEPTED |

|---|---|

Halifax Japanese Fund |

11:59hrs Friday 26th April 2024 |

| Scottish Widows Japan Growth | 17:00hrs Wednesday 24th April 2024 |

| Scottish Widows Japan Equity | 17:00hrs Wednesday 24th April 2024 |

Any investors in these OEICs, including those invested via an ISA, who want to buy or sell ahead of the second market closure should submit their instructions before the following cut off points:

| FUND NAME | DATE FOR CLIENT INSTRUCTION TO BE ACCEPTED |

|---|---|

Halifax Japanese Fund |

11:59hrs Thursday 02nd May 2024 |

| Scottish Widows Japan Growth | 17:00hrs Tuesday 30th April 2024 |

| Scottish Widows Japan Equity Fund | 17:00hrs Tuesday 30th April 2024 |

Following a review of our fund range as part of our 2022 Assessment of Value report, we’ve considered the options to improve outcomes for investors and intend to close 9 funds in our range. We are therefore proposing fund mergers to investors in those funds.

We believe the outcome of the merger proposal is in the interests of our investors, as the funds have not delivered value as intended in accordance with their investment objectives.

These proposed changes require approval from OEIC and ISA investors in the funds. We’re therefore mailing investors with details of the change and asking them to vote. To make the proposed changes, we need approval from 75% of the investors who vote.

If investors approve the proposal:

We don’t expect that the merger will constitute a disposal of Shares in the Merging Fund for UK capital gains tax purposes. Relevant clearances from HMRC have been received.

The tables below provide key dates and details of the impacted funds along with links to the relevant Voting Documents which provide detailed information on our proposed changes.

| Merging Fund Name | ICVC | Receiving Fund Name | ICVC | Voting Document | EGM Date and Time |

|---|---|---|---|---|---|

UK Select Growth Fund |

Scottish Widows UK and Income Investment Funds ICVC | UK Equity Tracker Fund | Scottish Widows Tracker and Specialist Investment Funds ICVC | 37709 (PDF, 217KB) | 10:00am 18/4/2024 |

| UK Smaller Companies Fund | Scottish Widows Tracker and Specialist Investment Funds ICVC | UK Equity Tracker Fund | Scottish Widows Tracker and Specialist Investment Funds ICVC | 37710 (PDF, 283KB) | 10:10am 18/4/2024 |

| European Select Growth Fund | Scottish Widows Overseas Growth Investment Funds ICVC | Global Select Growth Fund |

Scottish Widows Overseas Growth Investment Funds ICVC | 37711 (PDF, 275KB) | 10:20am 18/4/2024 |

| Adventurous Growth Fund | SW Income and Growth Funds ICVC | Progressive Growth Fund | Scottish Widows Income and Growth Funds ICVC | 37712 (PDF, 285KB) | 10:30am 18/4/2024 |

| Ethical Fund | Scottish Widows UK and Income Investment Funds ICVC | Environmental Investor Fund | Scottish Widows UK and Income Investment Funds ICVC | 37717 (PDF, 220KB) | 10:40am 18/4/2024 |

| Merging Fund Name | ICVC | Receiving Fund Name | ICVC | Voting Document | EGM Date and Time |

|---|---|---|---|---|---|

| Smaller Companies Fund | HBOS Specialised Investment Funds ICVC | UK Equity Tracker Fund | HBOS UK Investment Fund ICVC | 37714 (PDF, 196KB) | 11:00am 18/4/2024 |

| Special Situations Fund | HBOS Specialised Investment Funds ICVC | UK Equity Tracker Fund | HBOS UK Investment Fund ICVC | 37715 (PDF, 270KB) | 11:10am 18/4/2024 |

| Fund of Investment Trusts | HBOS Specialised Investment Funds ICVC | International Growth Fund | HBOS International Investment Funds ICVC | 37716 (PDF, 276KB) | 11:20am 18/4/2024 |

| Ethical Fund | HBOS Specialised Investment Funds ICVC | International Growth Fund | HBOS International Investment Funds ICVC | 37713 (PDF, 279KB) | 11:30am 18/4/2024 |

Detailed Fund Information

To access the latest investment documentation for the funds, for example Key Investor Information Documents (KIIDs), Supplementary Investor Information Documents (SIIDs) and prospectuses please visit :

Scottish Widows funds

Halifax funds.

You can find the new KIID for the Scottish Widows UK Equity Tracker Fund Class A Accumulation fund here (PDF, 852KB).

You can find information on Halifax ISA Terms & Conditions here (PDF, 302KB).

Some of our Life and Pension customers invest in Life and Pension funds which currently invest in the underlying funds shown in the table above and are therefore affected by this change. The underlying funds shown in the table above are expected to close on 24th June 2024. This means we need to make some changes to these Life and Pension funds.

The affected Life and Pension funds will have new investment aims from 24th June 2024 and their names will change in the future (PDF, 195KB). We’ll add the date here as soon as it’s available. Customers may continue to see the old fund names on communication we send until the names are updated. We’re writing out to let our impacted Life and Pension customers know about these changes. Here you can find full details of the aims and risks (PDF, 311KB) of each fund.

Life and Pension customers don’t need to do anything if they believe the change meets their investment needs and objectives after the changes. It’s important to review the changes to the way the Fund will be invested and the associated risks.

We regularly review our SW Life and Pension funds to ensure they remain appropriate to customers.

From 31st May 2024 we’re closing the following:

These shouldn’t be considered for investment.

We’ll write to you if you’re invested in this fund because we need you to choose a new investment option. If you don’t choose one, we’ll move the value of your investment to another investment option on your behalf, along with any ongoing contributions you make to the closing Fund.

The fund reduced its equity exposure (the amount the fund invests in shares) at the start of 2024. The adjustment ensures the fund stays aligned to its balanced risk profile and naming convention. We did not write to individual customers about this change because the fund’s primary objective and mandate did not change.

The objective description has been enhanced via the factsheet to make it clearer for customers. It continues to aim for long term growth through a mix of equities, bonds, property and cash. The fund is now more closely aligned with balanced risk expectations and similar funds of that nature.

We’ve reviewed the SW Life and Pension Funds listed below and decided to close them.

These Funds shouldn’t be considered for investment.

If you’re currently invested in one or more of these Funds, we’ll write to you because we need you to choose a new fund or funds. If you don’t choose a new fund or funds, we’ll move the value of your investment into another fund on your behalf, along with any ongoing contributions you make to the closing Funds.

The Scottish Widows Multi-Manager Diversity Fund and the Scottish Widows Multi-Manager Select Boutiques Fund will close on or around 16th June 2023.

These funds wholly invest in underlying funds managed by the fund manager, abrdn Fund Managers Limited.

Following a decision made by the fund manager to merge its underlying funds, we’ve decided to close the SW Life and Pension Funds that invest in them.

If you’re currently invested in one, or both, of these closing funds, we’ll write to you to let you know about the changes to your investment.

These SW Life and Pension Funds are no longer open for investment to new customers.

We’ve reviewed the SW Life and Pension Funds and have decided to close some of them to the products we’ve shown below. This affects customers whose plan number begins with ZU. The closing funds shouldn’t be considered for investment.

If you’re currently invested in one or more of these funds, we’ll write to you to ask you to choose a new investment option. If you don’t choose a new option, we’ll move the value of your investment in the closing funds into a replacement investment option on your behalf. We’ll also move any ongoing contributions being paid to the closing funds.

Scottish Widows Group Stakeholder Plan

Scottish Widows Retirement Saver

Scottish Widows Group Transfer Plan

Japan’s financial markets close on various days throughout the year to mark national holidays. In May, the holidays fall on 3 consecutive days from Wed 3rd to 5th May 2023.

What this means for customers

OEICS and ISAS

Our three Japanese OEIC funds, which invest exclusively in Japanese equities, will be unavailable for trading on these dates. These funds are:

Any investors in these OEICs, including those invested via an ISA, who want to buy or sell ahead of the market closure should submit their instructions before the following cut off points:

FUND NAME DATE FOR CLIENT INSTRUCTION TO BE ACCEPTED

Halifax Japanese Fund 11:59hrs Tuesday 2nd May 2023

Scottish Widows Japan Growth 17:00hrs Friday 28th April 2023

Scottish Widows Japan Equity Fund 17:00hrs Friday 28th April 2023

We’ve reviewed the SW Life and Pension Funds and have decided to close some of them to the products we’ve shown below. This affects customers whose plan number begins with ZU. The closing funds shouldn’t be considered for investment.

If you’re currently invested in one or more of these funds, we’ll write to you to ask you to choose a new investment option. If you don’t choose a new option, we’ll move the value of your investment in the closing funds into a replacement investment option on your behalf. We’ll also move any ongoing contributions being paid to the closing funds.

Scottish Widows Retirement Saver

Scottish Widows Group Stakeholder Pension Plan

Scottish Widows Group Transfer Plan

HSBC are merging investments in the YCGBP share class of the Islamic Global Equity Index Fund (‘the Fund’), into their Irish domiciled HSBC UCITS Common Contractual Fund (the ‘CCF Fund’) on 18th November 2022.

The CCF Fund is also an Islamic themed Global Equity fund. The merger attracts the benefit of tax transparency for the new CCF Fund.

The Scottish Widows Specialist Global Equity fund series, below, currently invest in the Fund. There will be no changes, or additional charges for customers invested in the SW pension fund series because of this merger, as the new CCF Fund has a similar aim and risk profile to the Fund.

You can find more information on the Scottish Widows Specialist Global Equity fund in the Scottish Widows Pension Funds Investor’s Guide (PDF, 1MB), or the Scottish Widows Life Funds Investor’s Guide (PDF, 627KB). Or you can ask us for more information.

WHAT THIS MEANS FOR CUSTOMERS WHOSE PLANS BEGIN WITH ZU

The funds below also currently invest in the Fund. There will be no changes, or additional charges for customers invested in those funds as a result of this merger, as the new CCF Fund has a similar aim and risk profile to the Fund.

Customers invested in the funds listed can find more fund information on their scheme info site.

Atlas Shariah Compliant Fund s1

Atlas Shariah Compliant Fund S10

Atlas Shariah Compliant Fund s2

Atlas Shariah Compliant Fund s3

Atlas Shariah Compliant Fund s4

Atlas Shariah Compliant Fund s5

Atlas Shariah Compliant Fund s6

Atlas Shariah Compliant Fund s7

Atlas Shariah Compliant Fund s8

Atlas Shariah Compliant Fund S9

EDFG (ex BEGG) Shariah

EDFG (ex EEGS) Shariah

EDFG (ex EEPS) Shariah

Endsleigh HSBC Islamic CSW

HSBC Islamic 12 SW

HSBC Islamic 16 SW

HSBC Islamic 2 SW

HSBC Islamic SW10

HSBC Islamic SW11

HSBC Islamic SW13

HSBC Islamic SW14

HSBC Islamic SW15

HSBC Islamic SW18

HSBC Islamic SW20

HSBC Islamic SW22

HSBC Islamic SW7

Mercer EY Shariah SW25

Mercer Shariah

Mercer Shariah SW16

Passive Shariah

RMPP AVC Shariah Law

RSPCA Shariah Equity

Scottish Widows Shariah CS8

Scottish Widows Shariah CS7

Shariah

Shariah 1

Shariah CSW

Shariah Fund V

Shariah law (index tracker) DC

Shariah law (index tracker)

SW HSBC Islam 29

SW HSBC Islamic CS1

SW HSBC Islamic 1

SW HSBC Islamic 5

SW HSBC Islamic M

SW HSBC Islamic N

SW Mercer EY Shariah 26

SW Mercer Shariah 27

SW Mercer Shariah CS1

SW Shariah CS1

Tarmac Shariah

Following a review of the Managed Growth Fund (MGF) 4 and Managed Growth Fund (MGF) 6 asset allocations the Investment Association mixed asset sectors aligned to both funds have now changed as follows:

MGF 4 - The fund was previously aligned to the “Mixed Investment 20-60% Shares Sector" but is now aligned to the "Mixed Investment 40-85% Shares Sector"

MGF 6 - The fund was previously aligned to the “Mixed Investment 40-85% Shares Sector” but is now aligned to the “Flexible Investment Sector”

These changes are reflected in the published prospectus for MGF 4 & 6.

We’ve reviewed the SW Life and Pension Funds listed below and decided to close them.

These funds shouldn’t be considered for investment.

If you’re currently invested in one or more of these Funds, we’ll write to you because we need you to choose a new fund or funds. If you don’t choose a new fund or funds, we’ll move the value of your investment into another fund on your behalf, along with any ongoing contributions you make to the closing Funds.

We’ve reviewed the SW Life and Pension Funds listed below and decided to close them. We’re doing this because of significant changes being made to the underlying funds that the closing Funds invest in.

From 1st September you’ll no longer be able to invest in these Funds.

If you’re invested in one or more of these Funds already, we’ll write to you as we need you to choose a new fund or funds by 18th November 2022 or the value of your investment in the closing fund will be moved to an alternative fund on or around 25th November 2022.

Our full range of funds are given in our Fund Guides at www.scottishwidows.co.uk/lifefundsguide and www.scottishwidows.co.uk/pensionfundsguide

Aviva Investors have informed us that they are closing the Aviva Investors High Yield Bond Fund (the ‘underlying fund’) on the 19th of July. The four SW life and pension fund series noted below currently invest in the underlying fund. We will be closing them and moving customers’ investments and ongoing contributions to the SW High Income Bond Fund on the 13th of July. This note is for the Scottish Widows SW fund series listed below:

We will write to impacted customers. You can find more information on the Scottish Widows High Income Bond fund and our other funds in either the Scottish Widows Pension Funds Investor’s Guide (PDF, 1MB) or the Scottish Widows Life Funds Investor’s Guide (PDF, 616KB), or you can ask us for more information. Please check the fund changes webpage regularly as we’ll post any updates there.

To make it clearer how the funds are invested, we’re updating the fund aim for some of the Scottish Widows, Clerical Medical, Halifax and former Lloyds TSB Life and Pension funds.

The funds listed below invest directly in a Scottish Widows Unit Trust Managers Limited Open Ended Investment Company (OEIC) fund or HBOS Investment Fund Managers Limited OEIC fund. The updates to the fund aims for these funds were published in the funds’ factsheets for the end of May 2022 at www.scottishwidows.co.uk/fundfactsheets

An OEIC is a type of collective investment vehicle created to hold and manage assets on behalf of a number of investors. This detail is included in the funds’ aims.

| HALIFAX AND CLERICAL MEDICAL LIFE AND PENSION FUNDS |

|---|

| European Life Fund |

| European Pension Fund |

| Far Eastern Life Fund |

| Far Eastern Pension Fund |

| International Growth Life Fund |

| International Growth Pension Fund |

| Japanese Life Fund |

| Japanese Pension Fund |

| North American Life Fund |

| North American Pension Fund |

| Overseas Pension Fund |

| Pelican Life Fund |

| Pelican Pension Fund |

| Smaller Companies Life Fund |

| Smaller Companies Pension Fund |

| High Income Life Fund |

| High Income Pension Fund |

| UK Equity Income Life Fund |

| UK Equity Income Pension Fund |

| UK Equity Pension Fund |

| UK Growth Life Fund |

| UK Growth Pension Fund |

| SCOTTISH WIDOWS AND FORMER LLOYDS TSB LIFE AND PENSION FUNDS |

|---|

| Equity Pension Fund |

| European Life Fund |

| European Pension Fund |

| Formerly Lloyds TSB American Life Fund |

| Formerly Lloyds TSB American Pension Fund |

| Formerly Lloyds TSB Balanced Life Fund |

| Formerly Lloyds TSB Balanced Pension Fund |

| Formerly Lloyds TSB European Growth Life Fund |

| Formerly Lloyds TSB European Growth Pension Fund |

| Formerly Lloyds TSB Far Eastern Pension Fund |

| Formerly Lloyds TSB Income Life Fund |

| Formerly Lloyds TSB Japan Growth Life Fund |

| Pelican Life Fund |

| Pelican Pension Fund |

| Formerly Lloyds TSB Pacific Basin Life Fund |

| Formerly Lloyds TSB UK Equity Pension Fund |

| Formerly Lloyds TSB Worldwide Growth Life Fund |

| Global Equity Life Fund |

| Global Equity Pension Fund |

| Japanese Life Fund |

| Japanese Pension Fund |

| North American Life Fund |

| UK Equity Life Fund |

| UK Equity Pension Fund |

For the Life and Pension Tracker Funds listed below, the updates to the aims were published in the funds’ factsheets for the end of May 2022.

| LIFE AND PENSION TRACKER FUNDS |

|---|

| Halifax UK Index-Linked Gilt Fund |

| CM UK Index-Linked Gilt Fund |

| PM Index-Linked Gilt Tracker |

| Scottish Widows UK Fixed Interest Tracker Fund |

For the Life and Pension Funds invested in Scottish Widows Pooled Property ACS Fund 1, the updates to the fund aims have also been published in the funds’ factsheets

Clerical Medical UK Property Life Fund

Clerical Medical UK Property Pension Fund

Formerly Lloyds TSB Property Life Fund

Formerly Lloyds TSB Property Pension Fund

Halifax Property Life Fund

Halifax Property Pension Fund

Scottish Widows Property Life Fund

Scottish Widows Property Pension Fund

An Authorised Contractual Scheme (ACS) is a type of collective investment vehicle created to hold and managed assets on behalf of a number of investors.

The change to the aim won’t affect the funds’ risk profile and there won’t be a change to the annual management charge of these funds.

The SW Henderson UK Property funds shown in the table below (‘the SW funds’) were set up to invest in the Janus Henderson UK Property PAIF fund, which we sometimes refer to as the ‘underlying fund’. Following Janus Henderson’s decision to close the underlying fund, from 20th June, the SW Henderson UK Property funds will invest in the SWUTM Scottish Widows Pooled Property ACS Fund 1. Find out more about this fund.

Learn more about the closure of the Janus Henderson UK Property PAIF fund.

MAKING WITHDRAWALS FROM THE SW HENDERSON UK PROPERTY FUNDS

From 25th March we restricted certain sell transactions from the SW Henderson UK Property funds with some exceptions.

We’re lifting these restrictions from 20th June so customers invested in one or more of the SW funds can switch their investment in these funds to another fund or funds available to their product.

We plan to switch customers out of the SW Henderson UK Property funds to an alternative fund at a later date. If you’re invested in the SW funds at that time, we’ll write to let you know before we do this.

PAYING INTO THE SW HENDERSON UK PROPERTY FUNDS

The restrictions brought in from the 25th March will remain in place.

| FUND NAME |

|---|

| SW Henderson UK Property Life |

| SW Henderson UK Property Pension Series 1 |

| SW Henderson UK Property Pension Series 2 |

| SW Henderson UK Property Pension Series 4 |

We had intended to move the investment management of the following Scottish Widows Unit Trust Managers OEIC Funds from Aberdeen Asset Investments Limited to BlackRock Investment Management (UK) Limited in March 2022:

However, this change in investment management won’t now happen until a later date.

On 3rd May the benchmarks tracked by the funds moved to new screened benchmarks which align with our exclusions standard (PDF, 640KB).

Our Life and Pension Funds which invest in the above three OEIC funds will also change aim and benchmark to align them with the OEIC fund they invests in. These are:

You can learn more about these changes.

The SW Janus Henderson UK Property CS1 Fund (“the SW Fund”) invests in the Janus Henderson UK Property PAIF Fund (“the underlying fund”).

The fund manager, Henderson Investment Funds, has decided to close the underlying fund due to concerns that continued withdrawals could shrink it to a size where it’s no longer viable. Before closing the underlying fund and returning assets to investors, the fund manager decided it was in the interests of investors to suspend the underlying fund on 3rd March 2022 to safeguard the property portfolio for sale. We expect the underlying fund to close in the next month.

WHAT THIS MEANS FOR CUSTOMERS WHOSE PLANS BEGIN WITH ZU

We have written to customers whose plan number begins with ZU and who are invested in the SW Fund to explain that, to help protect their interests, we’ve applied restrictions to the SW Fund. Customers can’t currently buy, sell or switch units in the SW Fund.

The main exceptions to these restrictions are:

We encourage any customer with an immediate need to withdraw part or all of their investment to speak to us to understand what options are available at this time.

From 16th March 2022, any regular payments that would have been invested into the SW Fund have been redirected to the customer’s scheme’s default lifestyle strategy, and unless we receive an instruction before 3rd May 2022, we’ll move the value of their investment in the SW Fund to their scheme’s default lifestyle strategy after the underlying fund has closed.

Customers can ask to switch the value of their investment in the SW Fund into another fund or funds available to their plan. We’ll process instruction(s) after the underlying fund has closed. Details of the customer’s scheme’s default lifestyle strategy and the other investment options available are on their scheme info site. Here the customer can access Money4Life to redirect future payments to another fund or funds other than their scheme’s default option.

Customers should carefully consider the aims, risks and charges of funds before making any investment decisions.

On 29th April 2022 the appointed investment manager of the SW Mixed Investment and SW Flexible Retirement funds will change to Schroders from Ninety-One (previously known as Investec).

This strengthens our existing relationship with Schroders, with further operational benefits through integration, and allows us to better monitor day-to-day activities.

On receipt of the mandate, Schroders will make a small number of portfolio changes including:

The change will also allow us to begin a series of incremental improvements to the management and oversight of the funds over time.

If you’re invested in any of the following funds, there will be a 0.06% reduction in the Annual Management Charge from 29th April 2022.

| FUND | FACTSHEET |

|---|---|

| SW Mixed Investments CS1 | Factsheet (PDF, 184KB) |

| Scottish Widows Mixed Investments CS7 | Factsheet (PDF, 195KB) |

| Scottish Widows Mixed Investments CS8 | Factsheet (PDF, 182KB) |

| SW Flexible Retirement CS1 | Factsheet (PDF, 183KB) |

| Scottish Widows Flexible Retirement CS7 | Factsheet (PDF, 194KB) |

| Scottish Widows Flexible Retirement CS8 | Factsheet (PDF, 181KB) |

There are no changes to the:

Japan’s financial markets close on various days throughout the year to mark national holidays. In May, the holidays fall on 3 consecutive days from 3rd to 5th May 2022.

What this means for customers

OEICS and ISAS

Our three Japanese OEIC funds, which invest exclusively in Japanese equities, will be unavailable for trading on these dates. These funds are:

Any investors in these OEICs, including those invested via an ISA, who want to buy or sell ahead of the market closure should submit their instructions before the following cut off points:

| FUND NAME | DATE FOR CLIENT INSTRUCTION TO BE ACCEPTED |

|---|---|

| Halifax Japanese Fund | 11:59hrs Friday 29th April 2022 |

| Scottish Widows Japan Growth | 17:00hrs Thursday 28th April 2022 |

| Scottish Widows Japan Equity Fund | 17:00hrs Thursday 28th April 2022 |

Henderson Investment Funds has decided to close the Janus Henderson UK Property PAIF Fund (‘the Fund’) due to concerns that continued withdrawals could shrink the Fund to a size where it’s no longer viable. Prior to closing the Fund and returning assets to investors, it has decided it’s in the interests of investors to suspend the Fund now to safeguard the property portfolio for sale.

WHAT THIS MEANS FOR CUSTOMERS WHOSE PLANS BEGIN WITH ZU

If your plan number begins with ZU and you're invested in the Fund through the SW Janus Henderson UK Property CS1 fund you can learn more about how this affects your investment on the fund changes page. Please check this regularly as we’ll post any updates there.

WHAT THIS MEANS FOR RETIREMENT ACCOUNT FUND SUPERMARKET CUSTOMERS

If you're invested directly in the Janus Henderson UK Property PAIF Feeder I Acc Fund or Janus Henderson PAIF Feeder I Inc Fund through the Retirement Account Fund Supermarket, you can learn how this affects your investment at March: Funds suspended. Please check that page regularly as we’ll post any updates there.

What this means for other customers invested in our SW Henderson UK Property Life and Pensions Funds

The affected SW Henderson UK Property Life and Pension Funds (‘the SW funds’) are:

| FUND NAME |

|---|

| SW Henderson UK Property Life |

| SW Henderson UK Property Pension Series 1 |

| SW Henderson UK Property Pension Series 2 |

| SW Henderson UK Property Pension Series 4 |

Our SW Henderson UK Property life and pension funds invest in the Fund – we sometimes refer to the Fund as the ‘underlying fund’. Henderson’s decision to suspend and close the Fund means we need to take action on the SW funds to help protect our customers’ interests. We will write to all affected customers to explain the actions we’ve taken.

For as long as prices are published for the underlying Fund, we will continue to use those prices to value and price the SW funds. If prices stop being published for the Fund prior to its closure, we expect to use the last available published price for the Fund to value and price the SW funds.

We’ve imposed some restrictions on transactions into or out of the SW funds for all our customers and these are outlined below. At all times these restrictions will be in line with customers’ policy provisions and with their best interests in mind.

We expect to remove the restrictions on the SW funds once the underlying Fund is closed.

Despite Henderson’s decision to close the Fund, we may decide to keep our life and pension funds open by moving to invest in an alternative underlying fund or funds. If we do, we’ll confirm what that means for the funds and your investment in the funds.

MAKING WITHDRAWALS FROM THE SW HENDERSON UK PROPERTY FUNDS

From 25th March we’ve restricted certain sell transactions from the SW funds.

The main exceptions to these restrictions are:

We encourage any customer with an immediate need to withdraw part or all of their investment to speak to us to understand what options are available at this time.

PAYING INTO THE SW HENDERSON UK PROPERTY FUNDS

Any regular payments which are currently invested in the SW funds will continue to be invested in those funds.

From 30th March there are restrictions on other requests to invest payments in the SW Henderson Property life and pension funds. Specifically, we’re not accepting instructions to:

into the SW Henderson UK Property life and pension funds. If we receive any such requests, we’ll ask customers for an alternative investment instruction. If no alternative instruction is provided, we’ll refund or return the payment(s) as appropriate.

SWITCHES AND REDIRECTIONS INTO AND OUT OF THE SW HENDERSON UK PROPERTY FUNDS

We’re not accepting new instructions to switch into or out of the SW funds. Similarly, we’re not accepting new instructions to redirect payments into these funds.

The exception is our lifestyle strategies where investments will continue to be automatically switched into and out of the funds where applicable.

HOW LONG WILL THE SW HENDERSON UK PROPERTY FUNDS RESTRICTIONS LAST?

Henderson has suggested it intends on closing the Fund in around six weeks. This is an indicative timeline only.

We had intended to move the investment management of the following Scottish Widows Unit Trust Managers OEIC Funds from Aberdeen Asset Investments Limited to BlackRock Investment Management (UK) Limited in March 2022:

However, this change in investment management did not happen.

We are therefore delaying the planned changes to the benchmarks tracked by the funds whereby the funds were to move to new screened benchmarks which align with our exclusions policy.

We still plan to move the funds to new screened benchmarks and will provide updates on when this will happen.

Fund managers have suspended dealing in some funds, so we’ve had to restrict payments into and out of these funds. The suspended funds are listed below. We’re writing to all affected customers.

What this means for customers

If you’re invested in a suspended fund then you can’t currently buy, sell or switch units in the fund until the suspension is lifted. The trading restrictions were applied from the dates shown in the tables below.

If you gave us an instruction to buy, sell or switch units in a fund on or after the date it was suspended, it will not have been processed.

RETIREMENT ACCOUNT

Regular, single and transfer payments into a suspended fund will remain in the Control Account until we’re instructed otherwise by the customer or their adviser.

POLICIES BEGINNING WITH ‘ZU’

Regular, single and transfer payments into a suspended fund will be redirected to the cash account until we’re instructed otherwise by the customer or their adviser.

CONTROL ACCOUNT AND CASH ACCOUNTS

These options are not designed to be used as long-term investments. It’s important for customers to consider reinvesting payments redirected to these investment options in another investment fund or funds.

HOW LONG WILL THE TRADING RESTRICTIONS LAST?

The managers of the suspended funds aim to lift the suspensions when normal market conditions return. Once this happens, we’ll remove our restrictions and reinstate normal trading.

We’re unsure how long the suspensions will last. When they’re lifted, we’ll update this page to let you know.

You may want to watch our videos which cover stock market volatility.

| FUND NAME | SUSPENSION DATE |

|---|---|

| Liontrust Russia C Accumulation | 28.02.2022 |

| JPM Emerging Europe Equity Fund C - Net Accumulation | 28.02.2022 |

| Pictet Russian Equities I GBP Accumulation | 28.02.2022 |

| ASI Eastern European Equity Fund I Accumulation | 01.03.2022 |

| Barings Eastern Europe Fund I GBP Accumulation | 01.03.2022 |

| Jupiter Emerging European Opportunities I Accumulation | 01.03.2022 |

| ** Janus Henderson UK Prop PAIF Feeder I Acc | 07.03.2022 |

| ** Janus Henderson UK Prop PAIF Feeder I Inc | 07.03.2022 |

| Fidelity Emerging Europe, Middle East and Africa | 22.03.2022 |

** The fund manager has confirmed the Janus Henderson UK Property fund will close in the next few weeks due to concerns that continued withdrawals could shrink the fund to a size where it would no longer be viable. To safeguard the fund’s property portfolio for sale, the fund manager has decided to suspend the fund. We’ll write to you if you’re invested in the fund when it’s closed, and we know how the proceeds will be paid out.

| FUND NAME | SUSPENSION DATE |

|---|---|

| Liontrust Russia & Greater Russia C Accumulation GBP | 28.02.2022 |

| Jupiter Emerging European Opportunities | 01.03.2022 |

| ASI Eastern European Equity | 01.03.2022 |

Henderson Investment Funds has decided to close the Janus Henderson UK Property PAIF Fund (the Fund) due to concerns that continued redemptions could shrink the Fund to a size where it is no longer viable. Prior to closing the Fund and returning assets to investors, it has decided it is in the interests of investors to suspend the Fund now to safeguard the property portfolio for sale.

As a result, we’re unable to buy and sell shares in the Fund at this time.

The SW Henderson UK Property Life and SW Henderson UK Property Pension funds are invested in the Fund. We’re considering what action to take on these funds, and will provide an update here as soon as we can.

If you are invested in the Fund through the Retirement Account Fund Supermarket, you won’t be able to buy or sell shares in the Fund, including switches between funds, during the suspension period. Any regular investments you’ve asked us to make in the Fund will be redirected to your Control Account. You should consider how these amounts should be invested, and may want to take financial advice. Advisers normally charge for any advice given.

We’re reviewing our range of index tracking, (also referred to as passive), funds and making changes.

The changes are summarised here.

We’re aiming to make these changes on the dates we’ve given, but some of these changes may happen later. As we make the changes we’ll confirm the dates here. You can also call us for an update.

CHANGE OF INVESTMENT ADVISER

We’re changing the Investment Adviser (also referred to as the Fund Manager) for most of our index tracking/passive funds.

On 7th March 2022 BlackRock Investment Management (UK) Limited (BlackRock) will replace Aberdeen Asset Investments Limited. You can learn more about BlackRock at www.blackrock.com/uk

CHANGE OF THE FUNDS’ AIMS

The aims of some of our Life and Pensions (L&P) Funds are changing to align the wording with the Open Ended Investment Company (OEIC) fund they invest in – see section below on our index tracking OEIC funds for more detail. We sometimes refer to the OEIC fund as your L&P Fund’s underlying investment or fund. An OEIC is a type of collective investment vehicle created to hold and manage assets on behalf of a number of investors.

From 28th March 2022 we’re making changes to theour index tracking OEIC funds, listed further down, which some of our L&P funds invest in, so that they invest more responsibly and do not invest in companies which are involved in industries such as Controversial Weapons, Thermal Coal, Tar Sands and Tobacco. You can find out more at www.scottishwidows.co.uk/responsibleinvestment and in the section below on our index tracking OEIC funds.

THE LIFE AND PENSION FUNDS AFFECTED

| FUND NAME | CHANGE OF AIM | CHANGE OF INVESTMENT ADVISOR |

|---|---|---|

| Halifax UK FTSE 100 Fund | Yes | Yes |

| Halifax UK FTSE 100 Tracking Fund | Yes | Yes |

| Halifax UK FTSE 100 Pension Fund | Yes | Yes |

| St Andrews UK Index Tracker Life Fund | Yes | Yes |

| Formerly Lloyds TSB FTSE 100 Tracker Pension Fund | Yes | Yes |

| SW UK Equity Index Life Fund | Yes | Yes |

| SW UK Equity Index Pension Fund | Yes | Yes |

| SW UK Fixed Interest Index Tracker Pension Fund | No | Yes |

| Halifax Cautious Managed Life Fund* | No | Yes |

| Halifax UK FTSE All Share Fund | Yes | Yes |

| Halifax UK FTSE All Share Index Tracking Fund | Yes | Yes |

| Halifax UK FTSE All Share Pension Fund | Yes | Yes |

| SW UK All Share Tracker Pension Fund | Yes | Yes |

| PM UK Index Fund | Yes | Yes |

| Halifax UK Index-Linked Gilt Fund | No | Yes |

| CM UK Index-Linked Gilt Fund | No | Yes |

| PM Index-Linked Gilt Tracker Fund | No | Yes |

| SW Fundamental Index Global Equity Life Fund | Yes | Yes |

| SW Fundamental Index Global Equity Pension Fund | Yes | Yes |

| SW Fundamental Low Volatility Index Global Equity Life Fund | Yes | Yes |

| SW Fundamental Low Volatility Index Global Equity Pension Fund | Yes | Yes |

| SW Fundamental Index UK Equity Life Fund | Yes | Yes |

| SW Fundamental Index UK Equity Pension Fund | Yes | Yes |

| SW Fundamental Low Volatility Index UK Equity Life Fund | Yes | Yes |

| SW Fundamental Low Volatility Index UK Equity Pension Fund | Yes | Yes |

* At least 60% of the Fund is invested in actively managed fixed interest securities and a maximum of 40% is in shares (also known as equities) which are passively managed. The change of investment adviser only relates to the portion of the fund invested in shares.

The investment objectives and policies of some of our Open Ended Investment Company (OEIC) funds are changing. (An OEIC is a type of collective investment vehicle created to hold and manage assets on behalf of a number of investors.)

We’re changing the Investment Adviser (also referred to as the Fund Manager) for most of our index tracking, (also referred to as passive), funds.

The changes won’t affect the funds’ risks and there won’t be a change to the annual management charge as a result of this change.

CHANGE OF INVESTMENT ADVISER

On 7th March 2022, BlackRock Investment Management (UK) Limited (BlackRock) will replace Aberdeen Asset Investments Limited. You can learn more about BlackRock at www.blackrock.com/uk

We will retain ownership of the funds and will remain responsible for defining the funds’ investment objectives and policies, and the strict parameters on how the funds should be run. BlackRock’s performance will be regularly monitored.

CHANGES TO HOW THE FUNDS WILL INVEST

From 28th March 2022, once the appointment of the new Investment Adviser has been completed, some of the funds’ investments will change as we exclude companies involved in industries such as Controversial Weapons, Thermal Coal, Tar Sands and Tobacco. We will change the benchmark index of those funds and align the funds to their new benchmark index. These changes will be made by amendments to the investment objectives and policies of our impacted OEIC funds. You can find out more about how we are investing more responsibly at www.scottishwidows.co.uk/about_us/responsibleinvestment.

To invest the funds more responsibly they won’t invest in companies:

CHANGE OF BENCHMARK INDEX

Some of our funds will track a different benchmark index which excludes companies which are involved in industries such as, Controversial Weapons, Thermal Coal, Tar Sands and Tobacco.

A fund’s benchmark is an index, rate or equivalent measure used to assess the performance of the fund. Usually a market index or the average performance of similar investments, or a bank index rate are used as benchmarks.

THE FUND’S NAME

We’re changing the fund name for some of our funds to align them with the change of benchmark.

If you’re invested in one or more of these funds through an ISA Investor from HBOS Investment Fund Managers Limited then we’ve sent you updated ISA Terms & Conditions (T&Cs) which contain the changes made for any new fund names and benchmark index amendments. These T&Cs will apply once the changes have been made. Please keep them for your records as they will replace your existing T&Cs.

BUYING AND SELLING ASSETS AS A RESULT OF THE FUND CHANGES

The removal of investment in shares of companies in which we no longer wish to invest will result in a short-term increase in transaction costs. These will be borne by the fund itself. All other costs associated with this change will be paid for by us.

Transaction costs are incurred by our funds when investments are bought and sold. These can include broker fees and commissions charged for carrying out the trade, taxes incurred when buying and selling different types of investments. They are paid from the value of the fund and this is a normal part of the ongoing management for funds. These transaction costs are not included in the ongoing charge that appears on the Key Investor Information Document (KIID) for the fund.

We’re updating the investment objective and policy for these funds to reflect the changes. You can see these at www.scottishwidows.co.uk/funds

We’ve given below all our OEIC funds with a change of Investment Adviser along with any other changes we’re making:

| FUND NAME AT FEBRUARY 2022 | AMENDED FUND NAME FROM 28TH MARCH 2022 | CURRENT BENCHMARK INDEX AT FEBRUARY 2022 | BENCHMARK INDEX FROM 28TH MARCH 2022 |

|---|---|---|---|

| European (ex UK) Equity Fund | Developed Europe (ex UK) Equity Tracker Fund | MSCI Europe ex UK Index | FTSE Developed Europe ex UK Custom Screened Index |

| UK All Share Tracker Fund | UK Equity Tracker Fund | FTSE All-Share Index | FTSE All-Share Custom Screened Index |

| UK Tracker Fund | No change | FTSE 100 Index | FTSE 100 Custom Screened Index |

| UK Fixed Interest Tracker Fund | No change | No change | No change |

| UK Index-Linked Tracker Fund | No change | No change | No change |

| FUND NAME AT FEBRUARY 2022 | AMENDED FUND NAME FROM 28TH MARCH 2022 | CURRENT BENCHMARK INDEX AT FEBRUARY 2022 | BENCHMARK INDEX FROM 28TH MARCH 2022 |

|---|---|---|---|

| U.K. FTSE 100 Index Tracking Fund | UK Large Company Tracker Fund | FTSE 100 Index | FTSE 100 Custom Screened Index |

| U.K. FTSE All-Share Index Tracking Fund | UK Equity Tracker Fund | FTSE All-Share Index | FTSE All-Share Custom Screened Index |

| Cautious Managed Fund * | No change | N/A | N/A |

| UK Tracker Fund | No change | FTSE 100 Index | FTSE 100 Custom Screened Index |

| UK Fixed Interest Tracker Fund | No change | No change | No change |

| UK Index-Linked Tracker Fund | No change | No change | No change |

* At least 60% of the Fund is invested in actively managed fixed interest securities and a maximum of 40% is in shares (also known as equities) which are passively managed. The change of investment adviser only relates to the portion of the fund invested in shares.

We’re making changes to the management of our property funds. The changes are summarised here.

We’re aiming to make these changes on the date we’ve given, but some of these changes may happen later. As we make the changes we’ll confirm the dates here. You can also call us for an update.

On 29th April 2022, Schroders Investment Management Limited (Schroders) will replace Aberdeen Standard Investments as the Investment Adviser for our property funds. This includes our life and pension property funds which invest via the Scottish Widows Pooled Property ACS Fund 1 – see below. You can learn more about Schroders at www.schroders.com/uk

L&P FUNDS INVESTED IN SCOTTISH WIDOWS POOLED PROPERTY ACS FUND 1

An Authorised Contractual Scheme (ACS) is a type of collective investment vehicle created to hold and manage assets on behalf of a number of investors.

The change won’t affect the funds’ risk profile and there won’t be a change to the annual management charge as a result of this change.

Scottish Widows will retain ownership of the funds and will remain responsible for defining the funds’ aims, and the strict parameters on how the funds should be run. Schroders’ performance will be regularly monitored.

LIBOR (the London Inter-Bank Offered Rate) was phased out at the end of 2021. It was used to help determine interest rates on consumer and banking products – and was often used as a way to measure performance - called a benchmark - for certain types of investments.

Over the years, a number of problems with LIBOR came to light because of how it was determined. LIBOR was an estimated rate and not based on actual transactions – that is, a small group of banks estimated what they’d charge other banks to borrow money overnight. Because of how it was set, the LIBOR rate was vulnerable to technological, regulatory, and ethical failings that could lead to an unfair rate. That’s why the Financial Conduct Authority (FCA), the UK financial regulator, announced that LIBOR would be phased out.

Scottish Widows and our appointed investment managers used LIBOR as a benchmark on a number of funds, often for absolute return and liquidity funds. Throughout 2021, we reviewed where LIBOR was used and arranged to use different benchmarks going forward. In some cases, this meant a change to the fund objectives.

The changes were seamless and don’t impact the value of investments or the way our funds are run.

Any changes which we have made will be stated on the relevant fund factsheets.

No. If you’re invested in funds impacted by these changes you don’t need to take any action. All of the necessary changes have been made by our appointed investment managers, and our investment team will be monitoring the transitions to the new benchmarks.

As part of the regulatory move away from LIBOR benchmarks, we’ve modified the fund objectives of some Scottish Widows funds which invest directly in the BlackRock ICS Sterling Liquidity Fund to more closely align with the objective of the underlying BlackRock fund. Specifically, the reference to outperformance relative to the benchmark has been removed.

A number of Scottish Widows pension funds invest in BlackRock funds via BlackRock-run Aquila Connect pension funds. From the end of November 2021, some of these Scottish Widows pension funds will invest directly in the underlying BlackRock funds and will see a name change to reflect this (see table below). We’re essentially removing the Aquila Connect pension funds layer from the fund structure.

Fund factsheets and other literature will be amended in due course.

The money that will be invested in the underlying Blackrock funds is held independently by a custodian which reduces risk for customers and Scottish Widows compared to holding via the Aquila Connect pension funds, where the assets are legally owned by the pension company which runs those funds, BlackRock Life.

| Current fund name | New fund name |

|---|---|

| SW Aquila Corporate Bonds All Stocks Index | SW BlackRock Corporate Bonds All Stocks Index |

| SW Aquila Over 15 Years UK Gilt Index | SW BlackRock Over 15 Years UK Gilt Index |

| SW Aquila Index-Linked Over 5 Years Gilt Index | SW BlackRock Index-Linked Over 5 Years Gilt Index |

| SW Aquila European Equity Index | SW BlackRock European Equity Index |

| SW Aquila 50/50 Global Equity Index | SW BlackRock 50/50 Global Equity Index |

| SW Aquila Japanese Equity Index | SW BlackRock Japanese Equity Index |

| SW Aquila 60/40 Global Equity Index | SW BlackRock 60/40 Global Equity Index |

| SW Aquila US Equity Index | SW BlackRock US Equity Index |

| SW Aquila World Ex UK Equity Index | SW BlackRock World Ex UK Equity Index |

| SW Aquila UK Equity Index | SW BlackRock UK Equity Index |

| SW Aquila 30/70 Currency Hedged Global Equity Index | SW BlackRock 30/70 Currency Hedged Global Equity Index |

Customers may be invested directly into these funds, or indirectly if they form a component of another Scottish Widows fund. A company pension scheme may also use these funds under a different name.

We made changes to the fund aim of our Scottish Widows Environmental Fund, which took effect from 27th September 2021.

WHY HAVE WE MADE CHANGES?

We’re making the changes to better meet environmentally and ethically conscious investment needs whilst aiming to deliver positive investment outcomes. We’re increasing Environmental Fund investment in companies which are working towards or supporting a sustainable economy and investing a larger proportion into small to medium sized companies. We’re also clarifying how the funds are run and updating the environmental and ethical exclusions screening (companies are excluded if they’re involved in activities based on certain criteria, further details are provided below).

WHAT DOES THIS MEAN FOR YOU?

The changes don’t alter your annuity income, or any other aspects of your investments with us. You don’t need to take any action, but you should review whether your investment in the fund continues to meet your investment needs. If you’d like to switch funds you can do this free of switching charges.

FOR MORE INFORMATION

You can read more about all the changes in the new fund aim below.

The fund invests via the Scottish Widows Unit Trust Managers (SWUTM) Environmental Investor OEIC Fund. The Environmental Investor OEIC Fund aim is:

To provide capital growth by investing in companies showing a commitment to the protection and preservation of the natural environment. The Fund is actively managed by the Fund Manager who chooses investments with the aim of outperforming the FTSE All-Share Index by 3% per annum on a rolling 3 year basis before deduction of fees.

At least 80% will be invested in shares of UK companies, with up to 20% in international companies.

SWUTM defines screens for UK and International equity markets to prevent investment in specific companies or industry sectors* that are harmful to the environment. The Fund Manager, in selecting investments it believes provide attractive capital growth, will seek a mix of investment in companies whose specific products and services directly support or provide positive environmental outcomes or benefits together with companies from any industry sector which, in the Fund Manager’s opinion, demonstrate high standards regarding sustainable environmental practice.

In seeking companies whose products and services support positive environmental outcomes the Fund Manager will look to invest in:

Companies which demonstrate high standards regarding sustainable environmental practice may include those which:

The Fund will not invest in companies which: own reserves in; extract; produce; supply; generate; or receive revenue from fossil fuels. This includes thermal coal, gas, oil and tar-sands. It will also not invest in companies which receive revenue from nuclear energy including nuclear uranium mining, and the production and use of controversial weapons.

The Fund retains a level of portfolio diversification and risk management by investing typically in 30 to 60 holdings across different sectors* of the Index and in different market sizes. As a result the Fund’s performance may differ substantially from the Index.

*A sector is a business area, industry or economy which shares the same characteristics. Company shares are typically grouped into different sectors depending on the company’s business.

To give long-term capital growth by investing in primarily UK companies which show a commitment to the protection and preservation of the natural environment. The fund may also invest in international companies applying environmental commitment. The companies are selected according to a range of negative environmental screening criteria. ‘Negative screening’ means using a fund’s agreed screening criteria to exclude undesirable investments, such as shares in companies whose practices may be harmful to the environment.

We made changes to the fund aim of our Scottish Widows Ethical Fund, which took effect from 27th September 2021.

Why have we made the changes?

We’re making the changes to better meet ethical investment needs whilst aiming to deliver positive investment outcomes. We’re clarifying how the Fund is run and extending and updating the ethical exclusions screening (companies are excluded if they’re involved in activities based on certain criteria, further details are provided below).

We anticipate that approximately 10%-15% of the current holdings within the Fund will be substituted with alternative assets to align the Fund to the new investment policy. The transaction costs for this activity will be borne by the Fund itself and these are currently estimated to be approximately 0.05%-0.1% of the overall value of the Fund.

What does this mean for you?

The changes don’t alter any other aspects of your investments with us. You don’t need to take any action, but you should review whether your investment in the fund continues to meet your investment needs. If you’d like to switch funds you can do this free of switching charges.

For more information

You can read more about all the changes in the new fund aim below.

The fund invests via the Scottish Widows Unit Trust Managers (SWUTM) Ethical OEIC Fund. The Ethical OEIC Fund aim is:

To provide capital growth by investing in shares of UK companies that demonstrate ethical attributes and practices.

The Fund is actively managed by the Fund Manager who chooses investments with the aim of outperforming the FTSE All-Share Index (the “Index”) by 3% per annum on a rolling 3 year basis, before deduction of fees.

At least 90% of the Fund will invest in shares of UK companies, it may also include some international companies.

SWUTM defines an ethical screen which means that the Fund will not invest, or investment is limited, in certain industries or companies. This approach is taken with companies whose products or services contribute to: social problems; destruction of human life; human rights or labour abuses; environmental damage; animal testing for cosmetic purposes and irresponsible corporate practice.

After screening for ethical criteria the Fund Manager selects investments based on a company’s growth prospects, market valuation and business risks.

In addition the Fund Manager engages with investee companies to monitor their compliance with international standards and promote ethical practices. The Fund will also take into account companies that demonstrate their involvement in the community and that have transparent and accountable corporate policies.

The Fund retains a level of portfolio diversification and risk management by investing typically in 30 to 60 holdings across different sectors* of the Index and in different market sizes. As a result the Fund’s performance may differ substantially from the Index.

The Fund will not invest in companies involved in:

*A sector is a business area, industry or economy which shares the same characteristics. Company shares are typically grouped into different sectors depending on the company’s business.

To give long-term capital growth by investing in primarily UK companies that demonstrate ethical attributes and practices. The fund may also invest in international companies demonstrating ethical practices. The companies are selected according to a broad range of negative ethical screening criteria. ‘Negative screening’ means using a fund’s agreed screening criteria to exclude undesirable investments, such as shares in companies which sell weapons or tobacco.

We made changes to the fund aim of our Scottish Widows Multi-Manager UK Equity Focus Fund on 4th August 2021.

Why have we made the changes?

This fund itself invests through an OEIC fund. We’ve expanded the fund aim description to clarify how the fund is invested and managed. Scottish Widows determine how the fund is managed, in place of Aberdeen Standard Investments.

What does this mean for you?

The changes don’t alter any other aspects of your investments with us. You don’t need to take any action, but you should review whether your investment in the fund continues to meet your investment needs. If you’d like to switch funds you can do this free of switching charges.

For more information

You can read more about all the changes in the new fund aim below.

NEW Fund Aim – from 4th August 2021

The Fund aims to achieve long-term growth by investing in a select portfolio of mainly UK equities. The portfolio’s investments will be actively managed by a number of fund managers.

At least 80% of the Fund will invest in UK equities. The majority of these companies are those which are incorporated, or domiciled, or have a significant part of their business in the UK.

A portion of the Fund may be invested in overseas equities, cash, cash-like investments. The Fund will invest in equities through other funds known as collective investment schemes. These collective investment schemes may employ techniques such as the use of derivatives for investment purposes and efficient portfolio management, and stock lending.

Fund Aim – prior to 4th August 2021

Aberdeen Standard Investments defines this fund’s objective and determines how this fund is run.

The fund aims to achieve long-term growth by investing in a select portfolio of mainly UK equities. The fund will normally hold fewer stocks than our other Multi-Manager UK equity funds. The portfolio’s investments will be managed by a number of fund managers.

We made changes to the fund aim of our Scottish Widows Multi-Manager UK Equity Growth Fund on 4th August 2021.

Why have we made the changes?

This fund was invested through an OEIC, the SPW Multi-Manager UK Equity Growth Fund, which has closed. We’ve changed the fund to invest into another OEIC, the SPW Multi-Manager UK Equity Fund, and moved the investments from the closed OEIC into the SPW Multi-Manager UK Equity Fund.