Your pension in your pocket

Our app makes it easy to keep an eye on your pension and plan for the future.

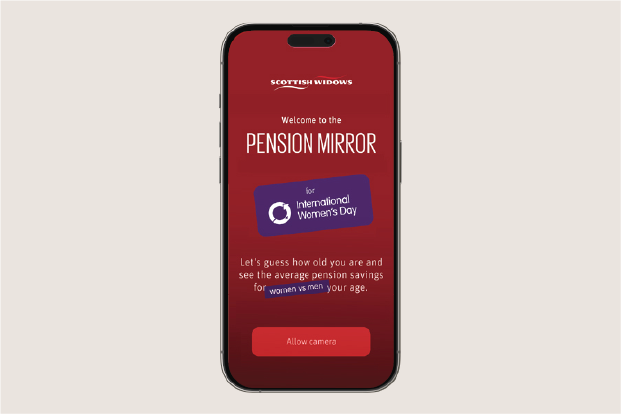

International Women’s Day 2024

On average, the gender pension gap jumps from £100 to £100,000 over a woman’s working life. This International Women's Day find out what’s driving such a huge difference in women and men’s pensions, and what you can do between the ages of 22 and 65 to help get pensions equality.

Find out what the pension gap is for your age, and how you can beat it.

The Pension Mirror will guess your age and how the average woman and man’s pension pots compare.

Let us guess your age.

Our Beat the Gap tool makes it personal, showing you when your own pension gap is most likely to occur and the top three ways you can help beat it.

See how you can Beat the Gap

The pension system is better suited to a more typically male pattern of working and savings. Things like pay inequalities, part time working and time off to manage childcare continue to make it harder for women to save as much across their working life and are the biggest drivers of the gender pension gap.

Although pay inequalities continue to exist, younger generations, especially women are saving for retirement earlier, 62% of women currently aged 22–29 said they started to save for retirement by the age of 25. This is good news but women still tend to earn less than men at all points in their working lives and as a result typically save less into their pension over this time.

After women have children the gap between their pension and a typical man’s starts to widen. For men, having children doesn’t normally impact their pension. This is because women tend to take on the lion’s share of childcare. Research tells us that 37% of mothers have left a job to cover childcare compared with 18% of fathers.

Employment breaks and part time working are big drivers of the gender pension gap. Earning less and potentially missing out on employer contributions into their pension, makes it harder for women to save enough for an equal retirement. 47% of mothers have gone part time to look after their children compared to 15% of fathers and men’s salaries are more likely to grow consistently over their working life.

Paying a bit more into your pension before children come along, could help lessen the financial impact of taking time off work later. If you’ve got a partner, you could agree how you'll balance the financial impact together by splitting childcare costs (women typically pick up the majority of these), sharing parental leave or asking them to top up your pension if and when you’re off work.

Saving into your pension in your 20s is your best opportunity to beat the pension gap because your money is invested for longer and has more time to grow. But to help you have the best chance of achieving pensions equality, women need to be saving more into their pensions than men. This is to offset any pay gaps and breaks in savings due to childcare (these impact women’s pensions more than men’s).

See the difference saving more can make.

Hopefully you’ll never need to think about pensions and divorce but it’s good to know what to consider just in case. Most divorces tend to happen in the mid to late 40s, by then men’s pensions are generally much higher in value than women’s, often due to less time out of work to raise children. Whilst family homes and joint savings are common parts of divorce agreements, pensions are split far less often. Divorce can typically cost women £77,000 at retirement so it's worth remembering to make pensions part of any discussions.

Have you paid money into a workplace pension years ago and forgotten all about it? If you have you could track it down using the Government's pension tracing tool at gov.co.uk. When you locate it, you might be able to combine it with any other pensions you have so they’re easier to manage.

You and your partner , if you have one should check your pension beneficiary details are up to date, this means naming the person you'd like your money to be left to. Scottish Widows customers can do this in the app or online. Make the most of the Governments free pensions guidance service - Pension Wise.

Pensions might not be front of mind when you’re in the thick of family life, but don’t forget about them. Chat with your partner about how you can share the financial impact of raising a family between you. Simple changes like splitting childcare costs (women typically pick up more of these), shared parental leave or asking your partner to top up your pension can help reduce the impact on your pension.

If you’re eligible for the State Pension, and you’ve taken time out of work to raise a family or care for a loved one, it may have impacted your State Pension entitlement if you didn’t claim child benefits or carers allowance to keep your National Insurance credits. Go to gov.uk to check your projected State Pension entitlement. If there's a shortfall, UK Taxpayers can pay in extra to fill any gaps until 5 April 2025.

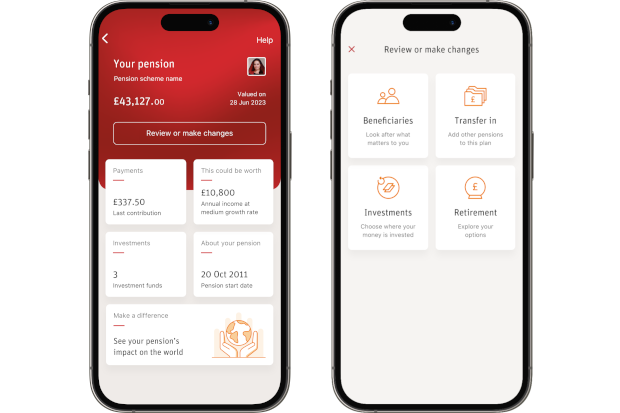

We can help you manage your savings and plan for the retirement you want with our online services and mobile app.

Your secure online account gives you access to your pension savings.

To help close the gap we’re working with organisations across our industry, the education sector and the Government. We’re committed to highlighting the issue, providing support and guidance as well as campaigning for pension reforms that could make it easier for women to save for retirement.

Our 5th International Women’s Day partnership helped shine a light on the gender pension gap. Our 2024 campaign brought our own data and expertise to life through our new Beat The Gap tool and social media.

We’re celebrating 20 years of industry leading research into Women & Retirement, the findings we use to lead the discussion and make recommendations to lobby for change. We champion making better pensions information and education material available for our scheme members and for all women.

We use platforms like International Women’s Day to raise awareness. We are proud to have been recognised at the 2024 Pension Age awards, winning the Diversity Award for our Women and Retirement activity.

Follow us on social for the latest updates