You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

Whatever your plans are for the future, it's important that you take time to think about the lifestyle you want to have.

How much do you need to have saved for the lifestyle you want? Do you have other sources of income that you could use in retirement?

Things to consider when working out how much you might need include:

Consider how long your pension needs to last. The UK average life expectancy for a 55 year old man is 84. For a 55 year old woman it's 87 (source: Office for National Statistics).

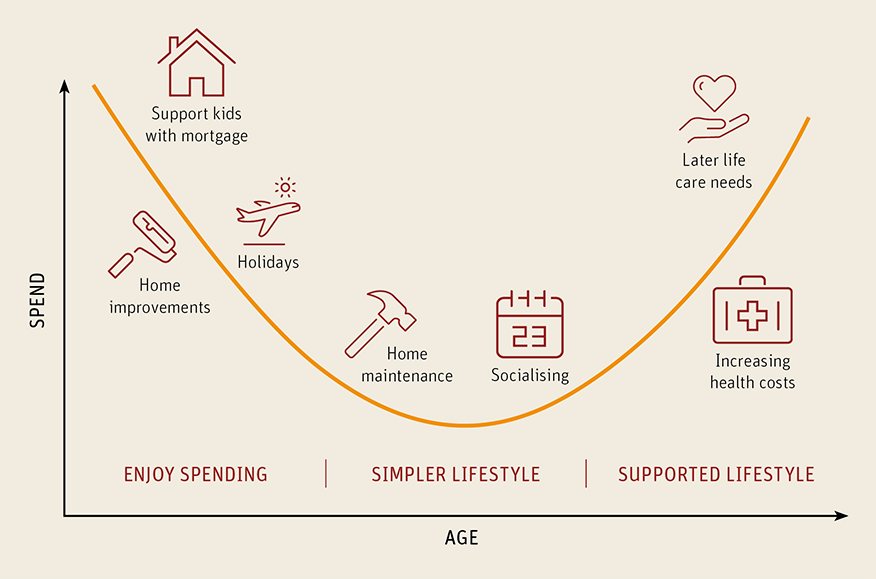

It's hard to know what you'll need in retirement, but it’s worth being prepared for changes in your spending. Some expenses might fall, like mortgage payments and commuting costs. Others can rise, such as care costs. So you need to factor this into your budget.

You can get a valuation of plans you have with us by logging in online. Or you could check your recent statement, or give us a call. The value of your pension can go down as well as up, and could fall below the amount(s) paid in.

You will only be able to receive the State Pension when you reach a certain age, and if you have paid enough National Insurance Contributions. See more on the State Pension

Consider any pensions you may have with other providers as you might want to think about combining them. You should also track down any lost pensions.

Once you know how much you have, take a look at our Retirement Calculator to see what you could get in the future.

Don’t forget, you can add to the income you’d get in retirement with other investments such as ISAs or OEICs, and any value in your property.

What you might expect to receive in your retirement may be affected by inflation. As living costs rise, the value of a fixed income goes down. Depending on how you decide to take your pension savings, you may be able to protect your income against the impact of inflation. Find out more about this in your pension options.

We hope this information has helped. We think you can never know enough when it comes to your pension, so for more information about shaping the future you want, go back to Understand more.

If you're ready to think about your pension options, take the next step.