Your pension in your pocket

Our app makes it easy to keep an eye on your pension and plan for the future.

Low cost investing means more of your money is working for you

Ways to invest

We've been investing for over 200 years, so we know what great value looks like. That's why our award-winning Stocks and Shares ISA has no annual account fees. Because when you invest for less, you're giving your money a better chance to grow.

From hands on to hands off, we’ve a range of investments and guidance to suit every kind of investor.

A carefully chosen range of funds, picked by our team of investment experts and designed to help you invest with confidence. Our Select List gives you a clear starting point for your investment goals.

IWeb Share Dealing is now Scottish Widows Share Dealing. The same great service, and now with:

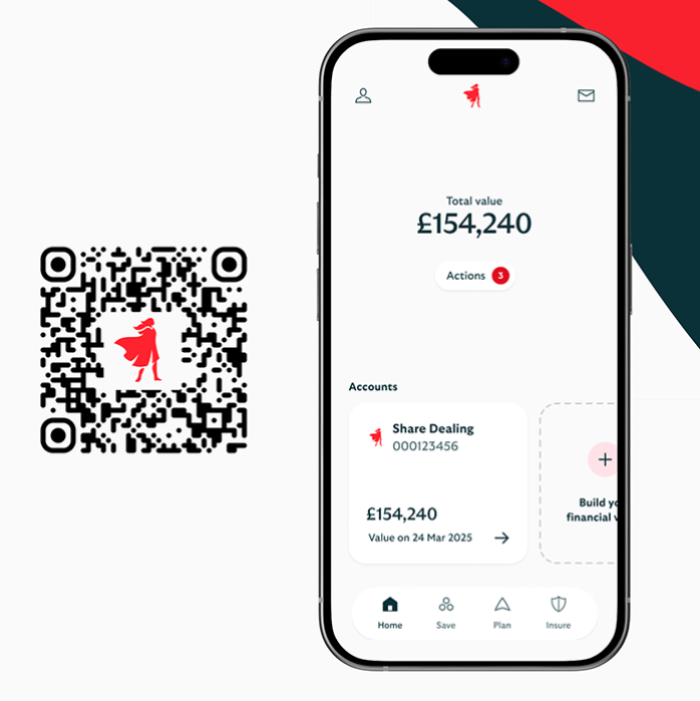

Already got the Scottish Widows app? Look out for Scottish Widows Share Dealing alongside your existing accounts in the app.

If you already have an account with Scottish Widows Share Dealing (formerly IWeb), log in to manage your investments.

Or manage your account in the app and start trading on the move today.

Personal pensions are another form of investing, which could suit you if you’re happy to leave your money invested for the longer term.

If you’re already getting the most out of your workplace pension, or if you don’t have a pension at all, our low cost personal pension options could be a good long-term option for you.

Take a hands-off approach with our Ready-Made Pension, and leave the decisions up to the experts.

Or if you’re comfortable doing your own research and like to be in control, our Self-Invested Personal Pension (SIPP) could help you reach your retirement goals.

Scottish Widows has been helping people prepare for the future since 1815. Today we remain as committed as ever to empowering our customers to make the most of their financial future.