You could win £10,000!

Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.

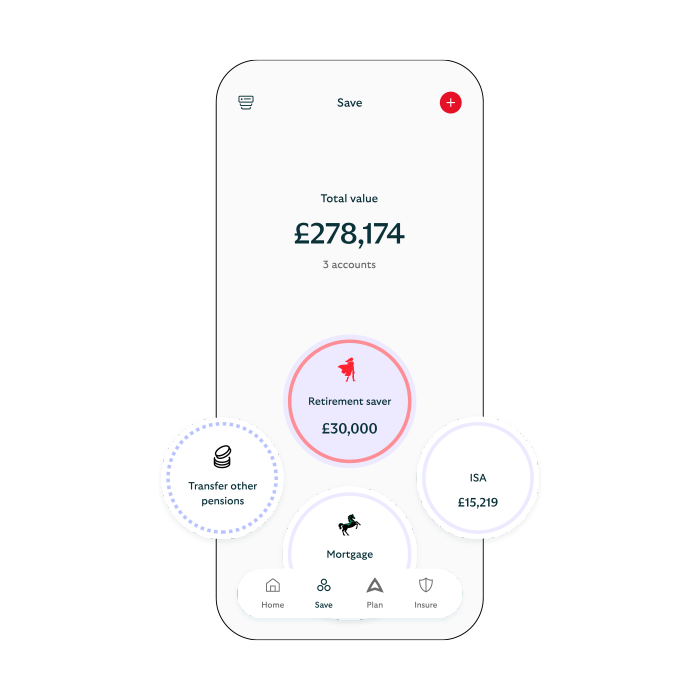

Turn pension fear into pension joy. We can help make things simple, so you can focus on what matters most to you.

Lots of us have pensions from old jobs. Bringing them together could make life easier.

New to pensions? Self employed? Our simple, personal pension makes it easier to start saving for your future.

A personal pension you set up yourself - take control of how your money is invested.

Did you know we have a range of games to help explain financial topics? Get hands-on with these interactive experiences and make learning about money simple and fun.

See your pensions, investments and insurance from Scottish Widows and other providers, all in one place.

Get started with just your National Insurance number.

You could win £10,000! Simply download, register and use the Scottish Widows app between 7 July and 31 December 2026. For full details and eligibility, or to opt out, see our terms and conditions.