Your pension in your pocket

Our app makes it easy to keep an eye on your pension and plan for the future.

See how you could benefit from offsetting

With an Offset Saver Account you could save money on your mortgage. On this page you can find out how it works, how you could benefit and how to apply.

YOU COULD LOSE YOUR HOME IF YOU DON'T KEEP UP YOUR MORTGAGE REPAYMENTS

The way our mortgage offset facility works is simple. A savings account (called an Offset Saver Account) is set up alongside your mortgage.

The money in your savings account is then ‘offset’ against your mortgage. So, while you won’t earn any interest on the savings in your Offset Saver Account, in effect you won’t be charged any interest on the same amount of your mortgage — as shown by the diagram below.

You can benefit from this in one of two ways:

With Reduced Term, while your monthly mortgage repayments stay the same each month (subject to changes in mortgage rates), the amount of mortgage interest you need to pay is lower due to your offset savings. More of your monthly mortgage payment is therefore used to repay the balance of your loan which effectively means you’re making mortgage overpayments each month. This could allow you to pay off your mortgage sooner and save money in interest.

How much sooner you pay off your mortgage is up to you. The more money you have in your Offset Saver Account the less interest you’ll be charged on your mortgage.

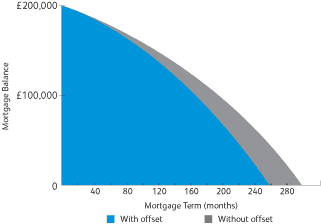

This example illustrates how you could benefit from the Reduced Term option.

Example based on a:

By offsetting, the term of the mortgage would be reduced by 3 years and 5 months, and £46,440 is saved in interest payments. The reduction of the mortgage term is illustrated in the diagram. In addition, there would be enough savings in the Offset Saver Account to repay the mortgage balance 7 years and 1 month early.

For more detailed information about offset, which we recommend you read, please see our Offset FAQs.

With this option, the term of your mortgage remains unchanged, but your monthly mortgage payment is reduced. This is because the offset benefit you earn each month from the savings in your Offset Saver Account is in effect used to reduce how much mortgage interest you pay the following month.

This means your savings could give you more disposable income each month. And, in addition to reducing your monthly payment, you could also save thousands of pounds during the term of your mortgage.

We collect your mortgage one month in arrears, so it's important to remember the savings balance in one month will reduce the mortgage payment you make two months later. For example, the offset benefit accrued in April would reduce your mortgage payment for May, which would be collected on 1 June.

This example illustrates how the Reduced Monthly Payment offset option works:

Example based on a:

The column “Mortgage payment after offset benefit applied” shows how the Reduced Monthly Payment option reduces the monthly mortgage payment. In total, £23,673 would be saved in interest payments during the mortgage term, and there would also be a sufficient Offset Saver Account balance to repay the mortgage balance 24 months early.

| Month | Number of days | Mortgage payment date | Offset benefit earned | Offset benefit applied | Mortgage payment before offset benefit applied* | Mortgage payment after offset benefit applied** |

|---|---|---|---|---|---|---|

| 15 Jan to 28 Feb | 45 | 1st March 2022 | £107.57 | £0.00 | £1332.06 | £1332.06 |

| March | 31 | 1st April 2022 | £74.10 | £107.57 | £1005.30 | £897.73 |

| April | 30 | 1st May 2022 | £71.71 | £74.10 | £1005.30 | £931.20 |

| May | 31 | 1st June 2022 | £74.10 | £71.71 | £1005.30 | £933.59 |

| June | 30 | 1st July 2022 | £71.71 | £74.10 | £1005.30 | £931.20 |

| July | 31 | 1st August 2022 | £74.10 | £71.71 | £1005.30 | £933.59 |

* The first mortgage payment is bigger than the subsequent normal monthly mortgage payments because there is more mortgage interest due as the mortgage starts part way through the month.

** Your offset benefit will accrue from the day you deposit funds into your Offset Saver Account and each month it will be applied to the mortgage payment for the following month.

For more detailed information about offset, which we recommend you read, please see our Offset FAQs.

Summary Box Key Product Information for our Savings Account(s) |

|

|---|---|

Account name |

Offset Saver Account |

| What is the interest rate? | You won’t earn any interest on savings in the Offset Saver Account. Instead, you won’t be charged any interest on the equivalent amount of money on your mortgage. |

| Can Scottish Widows Bank change the interest rate? | No, because we don’t pay interest we can’t change the interest rate on this account. |

| What would the estimated balance be after 12 months based on £1,000 deposit? | As there’s no interest paid on the account, the balance at 12 months would remain at £1,000. This assumes that:

|

| How do I open and manage my account? | When you apply for your mortgage, there’s an option to select Offset. You can also apply for Offset at any time while your mortgage application is being processed. If your mortgage account is already open, you can fill in the Offset Saver Account application form.

|

| Can I withdraw money? |

|

| Additional information |

|

If you’ve chosen to offset, we’ll open an Offset Saver Account for you. You’ll be able to transfer money to and from your Offset Saver Account using the nominated account you selected when you applied for your Scottish Widows Bank mortgage.

You can use Internet Banking and telephone banking. If you selected Internet Banking at application stage, you’ll receive your Internet Banking login details by post. You can also see your mortgage balance and your Offset Saver Account balance by logging in to Internet Banking.

No, you won’t earn any interest on the savings in your Offset Saver Account. In effect, this means, you won’t be charged any interest on the equivalent amount of money in your mortgage. This also means there is no tax liability.

So, by reducing the interest payable on your mortgage your savings are in effect earning mortgage rate interest. If the balance of your Offset Saver Account is greater than the mortgage portion you have chosen to offset against, you won’t receive any credit interest on the difference between the two amounts. If this situation happens, we’ll write to you as you may like to open an interest bearing savings account or even pay off some or all of your mortgage balance.

Irrespective of your Offset Saver Account balance, each month you’ll continue to pay the full monthly mortgage payment. This means your offset benefit is effectively being used to make mortgage overpayments each month.

This will gradually reduce the mortgage balance, which then reduces the term of the mortgage and saves you money.

Your monthly mortgage payment will be reduced each month, based on the offset benefit you accrue from the balance of your Offset Saver Account.

Your offset benefit will accrue from the day you deposit funds into your Offset Saver Account and each month it will be applied to the mortgage payment for the following month. So, for example, the offset benefit earned from the savings in your Offset Saver Account for the month of March, will be deducted from your mortgage payment for the month of April (which we’ll collect on 1 May). This means your mortgage payment will vary most months.

If you have a repayment mortgage, you will always pay the capital amount each month as it is only the mortgage interest element of your payment that is reduced each month.

We’ll send you a payment change letter each month your payment changes, which you’ll receive at least ten working days before your next mortgage payment.

We’ll collect your first monthly mortgage payment on the first day of the month following the first full month after completion. For example, if your mortgage completes on 15 January your first mortgage payment will be on 1 March.

Your first payment will be bigger than your normal monthly mortgage payment because your normal payment just covers the month in which it’s due. However, a new mortgage often starts part way through a month. So, for example, if your mortgage completes on 15 January, your first mortgage payment would be on 1 March and would include the interest due from 15 to 31 January, in addition to the normal payment due for February.

In the above example, if you’ve chosen Reduced Monthly Payment as your offset benefit and you have savings in your Offset Saver Account from 15 January, then the benefit will accrue from that date. However, the first occasion your monthly mortgage payment reduces will be on 1 April. This means your offset benefit will accrue from the day you deposit funds into your Offset Saver Account and each month it will be applied to your mortgage payment for the following month.

We collect your mortgage payment one month in arrears. So, it’s important to remember that following your first payment, the savings balance in one month will reduce the mortgage payment you make two calendar months later. For example, offset benefit earned in April would reduce your May payment, which would be collected on 1 June.

Mortgage interest is calculated daily. To ensure that standard monthly mortgage payments don’t fluctuate each month, we divide 365 days by 12.

365/12 = 30.42

Therefore, every month your mortgage payment is based on 30.42 days.

If you have an interest only mortgage, your monthly mortgage payments may well be £0 for several months throughout the year. However, each month your accrued offset benefit will be applied to the mortgage payment for the following month. This means that, for a March mortgage payment that is collected on 1 April, the offset benefit applied to it will be from February (28 days). Therefore, if you are 100% offsetting, you’d still have:

30.42 days – 28 days = 2.42 days of interest to pay on 1 April.

Or, for a September mortgage payment that is collected on 1 October, the offset benefit applied to it will be from August (31 days). This would mean:

30.42 days – 31 days = 0.58 of accrued offset benefit we will store and add to next month’s (September) offset accrued benefit.

If you have a repayment mortgage, you will always pay the capital amount each month as it is only the interest amount that you can offset against.

No. If the savings balance in your Offset Saver Account is greater than the mortgage portion you are offsetting against, you won’t earn any additional interest.

In this scenario, you may want to consider paying off your mortgage balance, or transferring some money into an interest bearing savings account.

No, you can also benefit by saving regularly.

When your mortgage balance is no longer outstanding we'll automatically transfer the balance of your Offset Saver Account to your nominated account.

You can only offset against one rate / repayment method – at application stage you’ll need to choose which one.

You can open one Offset Saver Account.

Your savings are held in a completely separate account – called an Offset Saver Account. Although you are using your savings to reduce the balance of your mortgage for interest purposes you can access them at any time should you need the money.

We believe this gives you the best of both worlds:

Yes, choosing offset doesn’t affect the flexibility of making mortgage overpayments, subject to the Terms and Conditions of the mortgage you have chosen.

Because we don’t actually pay interest on offset savings balances, this means there is no tax liability. So, by reducing the interest payable on your mortgage your savings are in effect earning mortgage rate interest.

If your money was earning interest in a savings account, you would have to pay income tax on any interest earned in excess of the personal savings allowance. From 6 April 2016 the personal savings allowance is £1,000 for basic rate taxpayers or £500 for higher rate taxpayers. There is no personal savings allowance for additional rate taxpayers (those earning over £150,000).

YOU COULD LOSE YOUR HOME IF YOU DON'T KEEP UP YOUR MORTGAGE REPAYMENTS

Scottish Widows Bank is a trading name of Lloyds Bank plc. Registered office: 25 Gresham Street, London EC2V 7HN. Registered in England and Wales, no. 2065. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under number 119278.