Welcome to your Workplace Pension

Global Connections Retirement Savings Plan

Your pension information site film

Thanks for saving with Scottish Widows and trusting us to help you make the most of your financial future.

Your pension information site has lots of information to help you understand more about your pension.

Film running time under 2 mins.

How does a Workplace Pension work?

Your workplace pension is a long-term savings plan. Even if retirement feels like a long way off, the earlier you save, the more time your money has to grow.

If you pay money in, your employer may too. You'll also benefit from tax relief from the Government and potential investment growth. Tax benefits will depend on individual circumstances, but keep in mind that tax rules can change.

Film running time under 3 mins.

Retirewell webinar series

Join our pension experts for a programme of live webinars and get the chance to ask them anything about your workplace pension.

Important things to do

Keep track of your pension:

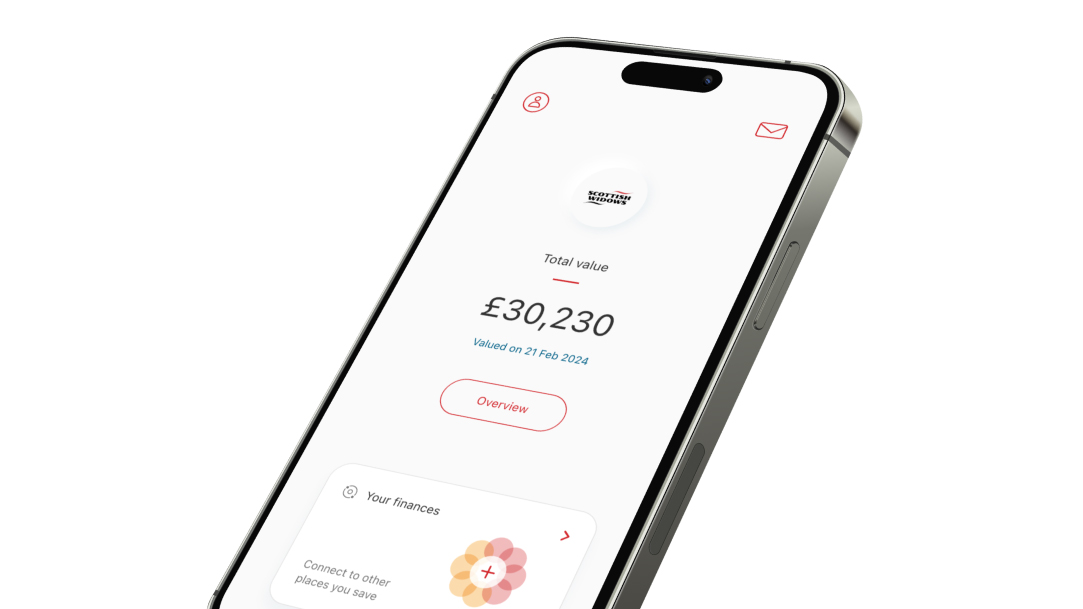

Use the Scottish Widows app or secure portal to manage your pension. It's important that you:

- keep your personal details up to date and provide us with your personal e-mail address so that we can keep in touch even if you change jobs

- nominate your beneficiaries so we know who you want your pension savings to go to if you die

- check that your selected retirement age is in line with when you plan to start accessing your pension savings.

Download our app

All you need is your:

- National Insurance number

- plan number or postcode

Beware of scams

Watch our film to find out how to spot a pension scam.

Film running time 1.5 mins.

Planning for your future

State Pension film

Watch our film on the State Pension to find out more.

Film running time 5 mins.

Plan for more than just retirement

Wills and power of attorney aren't just for later life - they're for peace of mind at any age.

We can help you get them sorted, so your wishes are clear and your loved ones and protected, whatever the future holds.

Find out more about will writing

Supporting vulnerable customers

This film explains the additional support services available to you through our partnerships. You can also learn more about these in our support guide (PDF, 1MB).

Film running time 2 mins.

Women and retirement

Scottish Widows Women and Finance Invest in You Hub brings together guidance, tools and products to help support women in building their financial future and closing the gender pension gap.

Tools & games

-

Use the calculator Opens third party site in a new tab

Our retirement calculator can help you find out what your income and lifestyle could be in retirement.

Having the value of any pensions, savings and investments you have will help you get the most out of the calculator.

-

Visit Power up Opens third party site in a new tab

Did you know Scottish Widows have a range of games available that help explain financial topics?

Get hands-on with interactive experiences and make learning about money simple and fun.

Library & resources

-

Below you will find information about your investment options and charges. You can make changes to where your pension savings are invested through the Scottish Widows app or by logging into your secure portal.

Global Connections Retirement Savings Plan information

Investments library and resources Your investment choices and charges (PDF, 200KB)

This short guide lists the pension fund choices available to you and the total annual fund charge for each fund.

Explore information on the alternative investment options available to you, past performance, their charges and their fund factsheets.

The following provides more information about how your pension savings are invested:

Investment choices and charges Introduction to investing (PDF, 3MB)

In this detailed guide you'll find information on how investing works, what a default investment option and lifestyling strategy is, as well as the different types of assets you can invest in and their risks.

If you want to keep up to date with the latest investment trends, or just learn about the basics, we’re here to help. We’ve got useful information and thoughts from our experts on the Exploring investments webpage.

Investments library and resources Guidance on your fund choices (PDF, 800KB)

This short guide provides information on the different fund choices that are available to you, including the various lifestyling strategies available.

Pensions Investment Approaches guide (PDF, 900KB)

Our Pension Investment Approaches (PIAs) are our fully governed range of investment strategies. In this detailed guide you’ll find details of the different options available to you.

We’re making changes to our Pension Investment Approaches (PIAs). For the latest information on the changes, please visit our customer page.

Scottish Widows Lifetime Investment (PDF, 2MB)

This guide explains how our Lifetime investment paths work.

We may have provided links to documents and other information supplied by third parties (which may include your employer or their advisers). They are solely responsible for their content and accuracy. All statements, views and opinions contained in these documents and other information are those of the third parties, not Scottish Widows.

-

The following guides can be used to help you think about your options:

Retirement options library and resources Helping You Prepare for Your Retirement (PDF, 1MB)

This detailed guide explains the options available to you when you want to start taking your benefits and the key things to consider before you do.

MoneyHelper guide - How to take your pension (PDF, 700KB)

This detailed guide from MoneyHelper also explains your retirement options, as well as the free retirement service that may be available to you through Pension Wise.

Things to Think About at Retirement (PDF, 100KB)

This short leaflet provides an overview of some of the key things to consider as you get closer to taking your pension benefits.

Taking benefits from your pension (PDF, 500KB)

This document details your retirement options and the step-by-step process to start your retirement.

Hub Financial Solutions - Annuity Service (PDF, 100KB)

This short guide, from the independent Hub Financial Solutions, explains the Annuity Service they provide. This service can help you select an annuity if you decide this is the right option for you and your needs.

The following guides explain your flexible income drawdown options:

Flexible income drawdown options library and resources This detailed guide explains how flexible income works, how we invest your savings and the risks associated.

Flexible Income Fund Range (PDF, 300KB)

This detailed guide gives you an understanding of the funds you can invest in if you wish to take a flexible income.

This detailed guide provides key information to help you understand our Investment Pathways and choose the right one for you if you decide to take flexible income.

We may have provided links to documents and other information supplied by third parties (which may include your employer or their advisers). They are solely responsible for their content and accuracy. All statements, views and opinions contained in these documents and other information are those of the third parties, not Scottish Widows.

-

Key Features and Terms & Conditions library and resources Key features of your plan (PDF, 300KB)

This detailed guide contains important information about your plan and how it works.

Key features illustration (PDF, 700KB)

This short illustration shows our standard charges and how they could affect what you might get back. Your actual charges may be different from those shown, please see your personalised illustration for details.

Terms and conditions (PDF, 400KB)

If you joined the pension scheme before 1 December 2025, these terms and conditions will continue to apply until we tell you otherwise.

Terms and conditions (PDF, 400KB)

If you joined the pension scheme on or after 1 December 2025, these are the terms and conditions that apply to your plan.

We may have provided links to documents and other information supplied by third parties (which may include your employer or their advisers). They are solely responsible for their content and accuracy. All statements, views and opinions contained in these documents and other information are those of the third parties, not Scottish Widows.

-

Useful information library and resources Pension tax (PDF, 3MB)

In this detailed guide, you'll find information on how current tax legislation affects how you save for retirement. There's information on the tax implications on your pension savings, including how tax relief works.

Pension transfer guide (PDF, 300KB)

This guide describes the potential benefits of transferring existing benefits to your Retirement Saver and highlights some of the things to consider.

Transfer in form (PDF, 1MB)

If you decide to transfer and don’t want to complete our online transfer journey, please complete this application form.

We may have provided links to documents and other information supplied by third parties (which may include your employer or their advisers). They are solely responsible for their content and accuracy. All statements, views and opinions contained in these documents and other information are those of the third parties, not Scottish Widows.

Contact us

-

When you speak to us, we’ll ask you for your plan number. This helps us to make sure you’re speaking to the right team. If you don’t have your plan number, we can still help you.

We will then ask you some security questions, so we can check who you are.

We want you to get the best service, so we may record your call for training purposes.

-